BEFORE THE ADJUDICATING OFFICER

SECURITIES AND EXCHANGE BOARD OF INDIA

[ADJUDICATION ORDER NO. Order/SM/DP/2022-23/25284-25292]

UNDER SECTION 15 I OF SECURITIES AND EXCHANGE BOARD OF INDIA ACT, 1992 READ WITH RULE 5 OF SECURITIES AND EXCHANGE BOARD OF INDIA (PROCEDURE FOR HOLDING INQUIRY AND IMPOSING PENALTIES) RULES, 1995

In respect of:

Sr. No. | Name of the Noticee | PAN/DIN |

1 | Highbrow Market Research Private Limited (ways 2 capital) | AACCH8077M |

2 | Shri Laxmikant Sharma | BNYPS4320M |

3 | Shri Mohit Chhaparwal | AGOPC0896Q |

4 | Shri Hemant Agrawal | AOBPA3520Q |

5 | Shri Swapnil Prajapati | BTWPP9571K |

6 | Shri Sunil Atode | DIN-07857476 |

7 | Shri Girish Kumar Pahwani | CILPP0738B |

8 | Shri Chandan Singh Rajput | AWYPR5207Q |

9 | Shri Rahul Trivedi | AQNPT9607R |

In the matter of

Highbrow Market Research Private Limited

______________________________________________________________________________ FACTS OF THE CASE

1. Securities and Exchange Board of India (hereinafter referred to as “SEBI”) conducted an inspection of M/s. Highbrow Market Research Private Limited on the basis of complaints received on SEBI Complaints Redress System (hereinafter referred to as “SCORES”) which revealed violations of provisions of SEBI (Investment Advisers) Regulations, 2013 (hereinafter referred as “IA Regulations”) & SEBI Circular CIR/OIAE/2014 dated December 18, 2014 by M/s. Highbrow Market Research Private Limited (hereinafter referred to as “Company”/ “Noticee 1”) and its directors namely, Shri Laxmikant Sharma (hereinafter referred to as “Noticee 2”), Shri Mohit Chhaparwal(hereinafter referred to as “Noticee 3”), Shri Hemant Agrawal (hereinafter referred to as “Noticee 4”), Shri Swapnil Prajapati ((hereinafter referred to as “Noticee 5”), Shri Sunil Atode (hereinafter referred to as “Noticee 6”), Shri Girish Kumar Pahwani ((hereinafter referred to as “Noticee 7”), Shri Chandan Singh Rajput (hereinafter referred to as “Noticee 8”), Shri Rahul Trivedi ((hereinafter referred to as “Noticee 9” and Collectively referred to as “Noticees”). It is noted that Noticee Nos. 2 to 9 are the Directors of Noticee No. 1 in the following manner:

Sr. No. | Name of the Noticee | Appointment Date | Cessation Date |

1 | Shri Laxmikant Sharma | 26.12.2011 | 01.04.2016 |

2 | Shri Mohit Chhaparwal | 26.12.2011 | 01.04.2016 |

3 | Shri Hemant Agrawal | 26.12.2011 | 01.07.2017 |

4 | Shri Swapnil Prajapati | 26.12.2011 | 01.07.2017 |

5 | Shri Sunil Atode | 23.06.2017 | 23.05.2018 |

6 | Shri Girish Kumar Pahwani | 23.06.2017 | 19.12.2018 |

7 | Shri Chandan Singh Rajput | 21.05.2018 | Till date |

8 | Shri Rahul Trivedi | 19.12.2018 | Till date |

APPOINTMENT OF ADJUDICATING OFFICER

2. SEBI had appointed Shri Prasanta Mahapatra as the Adjudicating Officer under Section 15I of Securities and Exchange Board of India Act, 1992 (hereinafter referred to as “SEBI Act”) read with Rule 4(1) of SEBI (Procedure for Holding Inquiry and Imposing Penalties), 1995 (hereinafter referred to as “Rules”) vide communique dated March 30, 2022 read with modified communique dated September 21, 2022 to enquire into and adjudge under Sections 15C, 15EB, 15HA and 15 HB of Securities and Exchange Board of India Act, 1992 (hereinafter referred to as “SEBI Act”), the alleged violations by the Noticees. Thereafter, Ms. Asha Shetty, Chief General Manager was appointed as Adjudicating Officer. Subsequently, the undersigned has been appointed as Adjudicating Officer vide revised communique dated December 14, 2022

SHOW CAUSE NOTICE, REPLY AND HEARING

3. Based on the findings by SEBI, Show Cause Notice(s) dated January 05, 2023 (hereinafter referred to as ‘SCN’) was issued to the Noticee under Rule 4(1) of the Adjudication Rules to show cause as to why an inquiry should not be held and penalty be not imposed on them under Sections 15C, 15EB, 15HA and 15 HB of SEBI Act for the alleged violation of the provisions of IA Regulations. The SCN, inter alia, alleged the following:

3.1 Noticees promised assured profit/ target return to their clients (terming them as “approachable profit”) under various pre-defined packages on the investments made by the clients. By promising unrealistic / exorbitant returns to its clients, despite fully knowing that all the investments in securities market are subject to market risk, Noticees have not been honest and has not taken due care in its dealings in the best interest of its clients. Thus, it was alleged that the Noticees have failed to act in a fiduciary capacity towards its clients, thereby violating Regulation 15(1) and Clauses 1 (honesty and fairness) and 2 (diligence) as specified under Third Schedule of Code of Conduct for Investment Adviser read with Regulation 15(9) of IA Regulations.

3.2 It was alleged that the Noticees had not been fair in its dealing with their clients by not being transparent about the fee charged to the client and had not been informed of all the charges upfront. It is further alleged that the Noticees had adopted unethical business practices/ modus operandi (promising assured returns, recouping losses, shifting the client to high price package claiming the package is beneficial for the client, etc). Therefore, it was alleged that the Noticees had failed in their responsibility to act in fiduciary capacity to their client which is entrusted upon them under Regulation 15 (1) of IA regulation and failed to abide by Code of Conduct under Regulation 15(9) of IA Regulations read with clause 1, 2, 5 and 6 of Code of Conduct for Investment Adviser.

3.3 Further, obtaining the advisory fees by not making adequate disclosure to the clients, by creating false and hypothetical circumstances of payment windows and seat booking slots and by forcing and threatening the clients to make the payments, if not done dire consequences would follow, the Noticees had carried out such business practices which were malafide and detrimental in the interest of its clients and retail investors at large. Such acts of the Noticees was a misrepresentation of the truth on its part. Such representation is therefore prima facie, fraudulent and is covered within the definition of “fraud” defined under regulation 2(1)(c) of PFUTP Regulations. Hence, it was alleged that the Noticees have violated the provisions of Regulation 3 (a), (b), (c) and (d), 4(1) and 4(2)(a),(k),(m),(s) of PFUTP Regulations read with Section 12A(a), (b) and (c) of SEBI Act, 1992.

3.4 Noticees did not adopt process for assessing the risk a client is willing and able to take but the process was adopted to enforce the will of the Noticees on clients and force them to take high risk products. The risk profile was also not communicated after risk assessment but the risk forms were sent to the clients and replies to the risk profile questionnaire was instructed to maximize the risk score. Therefore, it was alleged that Noticees have violated Regulation 16 of IA Regulations. It was, therefore, alleged that the Noticees had behaved deceptively with the clients by changing their risk profile as per their own whims to maximize its revenue which is in violation of regulations 3(a), (b),(c) and (d) of PFUTP Regulations read with section 12A(a),(b) and (c) of SEBI Act.

3.5 It was alleged that Noticees sold same advisory product/service more than once with overlapping subscription period. During such overlap period, the clients would be receiving duplicate advise/tips/messages and such duplicate tips/advice, if any, is of no use to the clients. This dishonest practice of the Noticees is completely unprofessional and unethical with a view to enhance service revenue and against the interest of the clients. It is therefore, alleged that the Noticees had failed in their responsibility to act in fiduciary capacity to its clients which is entrusted upon them under Regulation 15 (1) of IA regulation, and failed to abide by Clause 1 of Code of Conduct for Investment Adviser as mentioned in Schedule III read with regulation 15 (9) of IA Regulations

3.6 It was alleged that the Noticees did not do any financial planning of the client, did not consider client’s investment objective while offering advisory product/services and selling multiple advisory product/services thereby keeping their own interest before the interest of clients. Hence, it was alleged that the Noticees have not acted fairly, honestly and in the best interest of clients and have therefore, violated the provisions of Regulation 17 of IA Regulations.

3.7 From the analysis of complaints, it was alleged that Noticees were following a practice of obtaining details of relatives of the clients. These relatives were also treated as clients. The payment received from the primary client and services provided is then split among the relatives to show that the Noticees were not charging exorbitant fee from a single client. Thus, it was alleged that the Noticees have not only failed to maintain appropriate standard of conduct but also failed to act in fiduciary capacity to its client and hence, it was alleged that Noticees have violated Regulation 15 (1) of IA Regulations and failed to abide by Clauses 1, 2, 5 and 6 of Code of Conduct under Regulation 15 (9) of IA Regulations.

3.8 It was observed from the data obtained from the SCORES and examination of complaints, that Noticee No. 1 did not redress Investor grievances as per the prescribed timelines by SEBI. The reports of SCORES provide that till date 58 unique complaints were long pending against Noticee No. 1. It was therefore, alleged that Noticees have violated SEBI Circular CIR/OIAE/2014 dated December 18, 2014 read with regulation 21(1) (redressal of client grievances) of IA Regulations.

4. Noticee No. 7 replied to the SCN vide reply dated January 17, 2023 and submitted the following:

4.1 The noticee was appointed as a Research Analyst in the stock market. The Noticee acted as a research Analyst for 4 years out of which he worked as a director Research employee for one and a half years. In that the Noticee in role was limited to that of Research Analyst and was required to work and a specific duty was defined, namely, that he would be responsible for economical operations in the area of research and it’s related activities. As he had no knowledge of the day to day trading or any activity relating to the market. Noticee had set out in detail area of work as a Director Research and attended three board meetings and all the documents produced during the meeting did not show any irregularity. It was contended that the noticee had no access to any scheme committed by the company nor had any role to play in such activities. Noticee’s employment was confined only to the research and designated as a director for a limited period but in fact he was an employee and was getting a salary. The noticee was not involved in the day to day affairs of the company.

4.2 That, it is further submitted in this regard that there are various terms and conditions elaborated in the said agreement and is mentioned that the company does not provides any guaranteed profit service, contents of para Market and Other Related Risk “The client expressly agrees and acknowledges that all investments are subjected to market and other related risk and there is no assurance or guarantee, whether directly or indirectly, that the value of or return on investment will always be accretive.

4.3 That, it is further submitted that the clients are repeatedly reminded that the company does not provide any guaranteed or assured return and the said profit is to be seen in terms of service delivery tenure, another example of the same is a scroll that runs on the top of the website of the company dscapital.com 24 x 7 which reads «Stock & commodity investments are subject to market risk, Please read the offer document and Before registering check all the terms and conditions on the website, Highbrow Market Research Pvt. Ltd. Limited do not provide any profit sharing services, guaranteed services, DMAT facility , and the services which are not mention in the website.

4.4 That, it is further submitted that the company never takes a client on board without following the procedure laid down in the act and all the mandatory compliance of KYC, RPM, Suitability report and invoices were issued to all clients in addition mandatory disclaimers and disclosures were made beforehand in all the cases, as such the company has complied with all the statutory requirements under SEBI (IA) regulations 2013 contemplated under chapter III of the said regulations, further, there was ambiguity in the regulations themselves as to which services are allowed and which are not, there is no guideline or procedure laid down by the Hon’ble Board to either get a prior approval of the service model neither is there a template provided to give services in line of such template, in such a case the respondents have served their clients in best possible way as per their understandings, it is pertinent to note that due to such ambiguity in the said regulation of 2013 SEBI has recently made certain amendment in these regulation to regulate Investment Advisory activities in a better way. As such the noticee cannot be made responsible for the acts or omission of the board.

4.5 The Noticee has submitted it has never made any assurance of profit to anyone. It has submitted that for the one-time service charge, it will continue to render investment advisory services to the client till such time period that the “particular return” is achieved. The Noticee has admitted that the service provided by it will lapse once the “particular return”, as stated in the agreement, is attained by the client.

4.6 The Noticee has contended that it does not assure a “particular return” to its investors. Instead, it is committing to its clients that it will continue to provide investment advisory services to its clients till the time the “particular return” is achieved. The Noticee, being a registered SEBI intermediary, is well aware of the fact that all investments in the stock market are subiect to market risk and a particular return, or for that matter, any form of return on an investment cannot be guaranteed, no matter how long the period for which the investment is held or advice on that investment is offered to the client. The Noticee has further submitted that: There are some conditions made by party 1 to reduce market risk, which party 2 has to follow for getting particular return from the market. – Trade on all given calls by company through text massage, for our institutional pack. – Manage proper Target and Stop loss level given by our research team. – Follow all the instruction given by our executive during the service. – Go through all below instruction, guidelines and T&C to minimize your risk from market.” From the aforementioned excerpt of the submissions of the Noticee it appears yet again that a “particular return” is being assured if the client of the Noticee follows the “conditions” as reproduced above. Therefore, the Noticee through the use of such terms/ clauses, is committing to the client that (i) he/ she will achieve the particular return mentioned in the agreement by acting on the investment advice provided and following the “conditions” stated above in the excerpt and (li) the investment advice will be provided till the time such particular return has been achieved. I find that the commitment to the client that the service offered will continue till the “particular return” is achieved actually amounts to offering an assured / guaranteed return and is a conscious concealment of the fact that any return on an investment cannot be guaranteed as all investments in the securities market are subject to market risk. It is a reasonable probability that the capital deployed by the investor may get eroded as the investment advice provided by the Notice turns out to be incorrect due to market risk. There could be even more unpredictable market scenarios which could not have been foreseeable at the time of the Noticee entering into the purported agreements with its clients. Therefore, any intermediary, committing to deliver a “particular return” to the investors, is not at all acceptable. The Notice submits that it has mentioned about “risk factors” associated with the investments at some other part of the agreement. The said disclaimer does not negate the fact that the Noticee has offered its services to its clients on the basis of assured profit/ returns as is evident from the nomenclature and content of various “investment schemes” offered by the Noticee as already detailed above.

4.7 That, it is further submitted in this regard that there are various terms and conditions elaborated in the said agreement and is mentioned that the company does not provides any guaranteed profit service, contents of para Market and Other Related Risk are reproduced here for your reference “The client expressly agrees and acknowledges that all investments are subjected to market and other related risk and there is no assurance or guarantee, whether directly or indirectly, that the value of or return on investment will always be accretive…. the client expressly agrees and undertakes not to hold the Investment Advisor liable, financially or otherwise, in respect of the loss due to market risk.”

4.8 The Noticee has contended that it does not assure a “particular return” to its investors. Instead, it is committing to its clients that it will continue to provide investment advisory services to its clients till the time the “particular return” is achieved. The Noticee, being a registered SEBI intermediary, is well aware of the fact that all investments in the stock market are subiect to market risk and a particular return, or for that matter, any form of return on an investment cannot be guaranteed, no matter how long the period for which the investment is held or advice on that investment is offered to the client. The Noticee has further submitted that: There are some conditions made by party 1 to reduce market risk, which party 2 has to follow for getting particular return from the market.- Trade on all given calls by company through text massage, for our institutional pack. – Manage proper Target and Stop loss level given by our research team. – Follow all the instruction given by our executive during the service. – Go through all below instruction, guidelines and T&C to minimize your risk from market.” From the aforementioned excerpt of the submissions of the Noticee it appears yet again that a “particular return” is being assured if the client of the Noticee follows the “conditions” as reproduced above. Therefore, the Noticee through the use of such terms/ clauses, is committing to the client that (i) he/ she will achieve the particular return mentioned in the agreement by acting on the investment advice provided and following the “conditions” stated above in the excerpt and (li) the investment advice will be provided till the time such particular return has been achieved. I find that the commitment to the client that the service offered will continue till the “particular return” is achieved actually amounts to offering an assured / guaranteed return and is a conscious concealment of the fact that any return on an investment cannot be guaranteed as all investments in the securities market are subject to market risk. It is a reasonable probability that the capital deployed by the investor may get eroded as the investment advice provided by the Notice turns out to be incorrect due to market risk. There could be even more unpredictable market scenarios which could not have been foreseeable at the time of the Noticee entering into the purported agreements with its clients. Therefore, any intermediary, committing to deliver a “particular return” to the investors, is not at all acceptable. The Notice submits that it has mentioned about “risk factors” associated with the investments at some other part of the agreement.

5. Vide letter dated February 08, 2023, Noticee No. 3 submitted his reply to the SCN and submitted the following:

5.1 I became the Director of the Company on December 26, 2011 and my profile was mainly pertaining to the Human Resources and handling the tax profile of the employees.

5.2 My association with the company was for a period commencing from December 26, 2011 till April 01, 2016.

5.3 I was not involved in the management, operations and regular business of the company.

5.4 The details are not available with me and I am not in a position to provide the same, particularly because I have ceased to be associated with the company since April 2016.

6. Vide email dated February 10, 2023, Noticee No. 4 replied to the SCN and submitted that he was associated with the company from December 26, 2011 to June 30, 2017 and did not play any active role in the board of the company. His main work was related towards payroll of the employees and to plan activities and functions in the company. Therefore, SEBI may seek the relevant information directly from the company.

7. Vide letter dated February 13, 2023, Noticee No. 1 replied to the SCN and submitted the following:

7.1 it is submitted that Mohit Chhaparwal has been associated with the company since December 2011 and continued as Promotor till 01st July 2017 and had main role towards the decisionmaking process in the company. Reply submitted by Mr Mohit Chhaparwal is completely denied.

7.2 it is submitted that the said complaints are motivated and instigated only to prejudice the case of this Noticee, there is a fair chance that, competitors of this Noticee might have instigated the complainants to file such false and frivolous complaints. Further it is requested, that SEBI must investigate into the truth of such complaints. It is further requested that such complaints be referred to Ombudsman or Arbitration as mandated under IA Regulations.

7.3 It is submitted that Highbrow through its website ways2capital.com has publicly displayed the terms and conditions along with its disclaimer and disclosures which were always available to the clients worldwide through internet. It is further submitted that even all the documents including the MOUs, Payment receipts and email correspondence, clearly communicate to the client that the investments are subject to market risks and no assured profits are promised by Noticee herein. That with reference to paragraph 14,15 and 16, Highbrow has specified properly the terms and conditions on the MOU, Welcome Mail, Payment Receipts and also on website that the Highbrow never provide any sort of Guarantee and assurance of the profit. The Term Approachable Profit is also referred to the profit which cannot be taken as guaranteed and assured. Further, there is no reason, for SEBI to “cherry pick” such data clearly ignoring the terms “not assured/not guaranteed”. Further there is no reason for Ld. Authority to attach any additional meaning to the term “approachable profit” by reading it out of context. Also, the service tenure which is mentioned in the receipt which is either 20 days. 131 days or 181 days on minimum basis refers to the original tenure of the package which clients has subscribed but company was still open to provide complementary services at no extra cost if it is required. It must be noted here that, the service tenure was to be extended “if required”. This shows Companies openness to continue to provide service in the larger interest of its customer. The same need not be read as any assurance of any nature.

7.4 It is submitted that the linking the approachable profit with the fees charged in a reverse mode by simply attempting to ratio out the same may not be a senseful exercise. It appears that the said conclusion is drawn based upon a pre-existing notion and under a pre-fixed mandate. It is further submitted that assuming that the fee charged is 1/4th of the target/approachable profit and no other consideration is weighed in except the figure of approachable profit, even in that instance, the same is not violative of any regulation. The Noticee was always free to charge the fees as per its own merits. The only rider on the fees to be charged was that it was expected to be reasonable. Nothing is produced on record to show that the said fees are unreasonable.

7.5 Highbrow has never promised Also, Highbrow is having proper signed documents which states that Advisor Company is not giving any assurance or guarantee of Profit. The audio records produced by the said complainants are denied for being false, bogus and manufactured only to damage the good will and repute of the Noticee and only to extract monies from this Noticee. As the original call records of the company are no more available with the company, hence, this Noticee is not in a position to appropriately deal with the same. It is requested that the said call recordings not be taken as evidence as the same appears to be bogus and manufactured. Further it does not suit with the standards of the Evidence Act. Hence the same need not be allowed to influence the decision of the Ld. Authority.

7.6 Inspection of the documents may be provided.

8. Noticee Nos. 2, 3, 5-9 did not file any reply to the SCN. Vide common notice of personal hearing dated February 08, 2023, Noticees were granted an opportunity of personal hearing on February 15, 2023. Vide email dated February 13, 2023, Noticee No. 1 sought adjournment of the hearing for two weeks. Vide hearing notice dated February 14, 2023, Noticee No. 1 was granted a final opportunity of being heard on February 27, 2023. However, the other Noticees did not appear for the personal hearing granted to them.

9. Noticee No. 1 appeared for the hearing on February 27, 2023 and reiterated the submissions made vide reply dated February 13, 2023.

10. Further vide hearing Notice dated February 21, 2023, Noticee No. 2-9 were granted personal hearing on March 01, 2023. Noticee No. 3 appeared for the hearing on March 01, 2023 and reiterated the submissions made vide reply dated February 08, 2023. Noticee No. 3 submitted that he had no role in soliciting clients. Noticee No. 3 further submitted that he was merely working as Human Resources and tax specialist and his only interaction was with the Chartered Accountant appointed for the same. Noticee No. 3 further submitted that he was not reporting to anyone and everyone was handling their various departments.

11. Vide Notice of personal hearing dated March 03, 2023, Noticee Nos. 2, 4-9 were granted a final opportunity of hearing on March 09, 2023, however, the said Noticees failed to appear for the same.

12. Vide email dated March 06, 2023, Noticee No. 7 was granted an opportunity to inspect the documents on March 10, 2023. However, Noticee No. 7 failed to conduct the same. Subsequently, vide notice of personal hearing dated March 10, 2023, Noticee was granted an opportunity of final hearing on March 17, 2023. However, Noticee No. 7 did not appear for the same.

13. As the SCN and Hearing Notices-cum-reminder to reply to SCN to Noticee Nos. 2, 5-9 could not be served through SPAD, the same were published in Times of India and Loksatta, Indore edition on March 18, 2023, Noticee Nos. 2, 5-9 were granted final opportunity of hearing on March 23, 2023. However, Noticee Nos. 2, 5-9 neither filed any reply to the SCN nor appeared for the personal hearing granted to them.

CONSIDERATION OF ISSUES AND EVIDENCE

14. I have carefully perused the charges levelled against the Noticees in the SCN and the material / documents available on record. In the instant matter, the following issues arise for consideration and determination:-

I. Whether Noticees have violated provisions of IA Regulations and IA Regulations by–

a. promising assured/guaranteed returns to its clients;

b. Selling multiple packages to clients with threat of forfeiture and charged unreasonable and undisclosed fee;

c. manipulating the risk profiles of clients and has failed to conduct due diligence;

d. failing to abide by principles of Suitability;

e. splitting of fee among the relatives of the client and denied to acknowledge clients even after receiving payment and forcefully captured the card details;

f. Non redressal of Investor Grievances;

II. Do the violations, if any, on the part of the Noticees attract monetary penalty under Sections 15C, 15EB, 15HA and 15 HB of SEBI Act?

III. If so, what would be the quantum of monetary penalty that can be imposed on the Noticees after taking into consideration the factors mentioned in section 15J of the SEBI Act?

15. Before proceeding further, I would like to refer to the relevant provisions of the SEBI Act, PFUTP Regulations and IA Regulations:

SEBI Act

Prohibition of manipulative and deceptive devices, insider trading and substantial acquisition of securities or control.

12A. No person shall directly or indirectly—

- use or employ, in connection with the issue, purchase or sale of any securities listed or proposed to be listed on a recognized stock exchange, any manipulative or deceptive device or contrivance in contravention of the provisions of this Act or the rules or the regulations made thereunder;

- employ any device, scheme or artifice to defraud in connection with issue or dealing in securities which are listed or proposed to be listed on a recognised stock exchange;

- engage in any act, practice, course of business which operates or would operate as fraud or deceit upon any person, in connection with the issue, dealing in securities which are listed or proposed to be listed on a recognised stock exchange, in contravention of the provisions of this Act or the rules or the regulations made thereunder;

Regulation 3(a), 3(b), (c), (d) and Regulation 4 (1) of SEBI (PFUTP) Regulations, 2003.

3. Prohibition of certain dealings in securities

No person shall directly or indirectly—

- buy, sell or otherwise deal in securities in a fraudulent manner;

- use or employ, in connection with issue, purchase or sale of any security listed or proposed to be listed in a recognized stock exchange, any manipulative or deceptive device or contrivance in contravention of the provisions of the Act or the rules or the regulations made there under;

- employ any device, scheme or artifice to defraud in connection with dealing in or issue of securities which are listed or proposed to be listed on a recognized stock exchange;

- engage in any act, practice, course of business which operates or would operate as fraud or deceit upon any person in connection with any dealing in or issue of securities which are listed or proposed to be listed on a recognized stock exchange in contravention of the provisions of the Act or the rules and the regulations made there under.

4. Prohibition of manipulative, fraudulent and unfair trade practices

(1) Without prejudice to the provisions of regulation 3, no person shall indulge in a [manipulative,] fraudulent or an unfair trade practice in securities [markets]

[Explanation.–For the removal of doubts, it is clarified that any act of diversion, mutualisation or siphoning off of assets or earnings of a company whose securities are listed or any concealment of such act or any device, scheme or artifice to manipulate the books of accounts or financial statement of such a company that would directly or indirectly manipulate the price of securities of that company shall be and shall always be deemed to have been considered as manipulative, fraudulent and an unfair trade practice in the securities market.]

(2) Dealing in securities shall be deemed to be a [manipulative] fraudulent or an unfair Trade practice if it involves any of the following] :—

…

(k) disseminating information or advice through any media, whether physical or digital, which the disseminator knows to be false or misleading in a reckless or careless manner and which is designed to, or likely to influence the decision of investors dealing in securities;

…

(s) mis-selling of securities or services relating to securities market

Explanation – For the purpose of this clause, “mis-selling” means sale of securities or services relating to securities market by any person, directly or indirectly, by─

- knowingly making a false or misleading statement, or

- knowingly concealing or omitting material facts, or

- knowingly concealing the associated risk, or

- not taking reasonable care to ensure suitability of the securities or service to the buyer

Regulation 16 and 17 of SEBI (Investment Advisers) Regulations, 2013 Risk profiling.

16. Investment adviser shall ensure that,-

(a) it obtains from the client, such information as is necessary for the purpose of giving investment advice, including the following:-

- age;

- investment objectives including time for which they wish to stay invested, the purposes of the investment ;

- income details;

- existing investments/ assets;

(iv) risk appetite/ tolerance;

(vi) liability/borrowing details.

(b) it has a process for assessing the risk a client is willing and able to take, including:

- assessing a client’s capacity for absorbing loss;

- identifying whether client is unwilling or unable to accept the risk of loss of capital;

- appropriately interpreting client responses to questions and not attributing inappropriate weight to certain answers.

(c) where tools are used for risk profiling, it should be ensured that the tools are fit for the purpose and any limitations are identified and mitigated;

(d) any questions or description in any questionnaires used to establish the risk a client is willing and able to take are fair, clear and not misleading, and should ensure that:

- questionnaire is not vague or use double negatives or in a complex language that the client may not understand;

- questionnaire is not structured in a way that it contains leading questions. (e) risk profile of the client is communicated to the client after risk assessment is done;

(f) information provided by clients and their risk assessment is updated periodically.

Suitability

17. Investment adviser shall ensure that,-

(a) All investments on which investment advice is provided is appropriate to the risk profile of the client;

(b) It has a documented process for selecting investments based on client’s investment objectives and financial situation;

(c) It understands the nature and risks of products or assets selected for clients;

(d) It has a reasonable basis for believing that a recommendation or transaction entered into:

(i) meets the client’s investment objectives;

(ii) is such that the client is able to bear any related investment risks consistent with its investment objectives and risk tolerance;

(iii) is such that the client has the necessary experience and knowledge to understand the risks involved in the transaction.

(e) Whenever a recommendation is given to a client to purchase of a particular complex financial product, such recommendation or advice is based upon a reasonable assessment that the structure and risk reward profile of financial product is consistent with clients experience, knowledge, investment objectives, risk appetite and capacity for absorbing loss.

Regulation 21(1) of SEBI (Investment Advisers) Regulations, 2013 Redressal of client grievances.

21.(1) An investment adviser shall redress client grievances promptly.

THIRD SCHEDULE

Securities and Exchange Board of India (Investment Advisers) Regulations,2013

CODE OF CONDUCT FOR INVESTMENT ADVISER

1. Honesty and fairness

An investment adviser shall act honestly, fairly and in the best interests of its clients and in the integrity of the market.

2. Diligence

An investment adviser shall act with due skill, care and diligence in the best interests of its clients and shall ensure that its advice is offered after thorough analysis and taking into account available alternatives.

…

5. Information to its clients

An investment adviser shall make adequate disclosures of relevant material information while dealing with its clients.

3. Fair and reasonable charges

An investment adviser advising a client may charge fees, subject to any ceiling as may be specified by the Board. The investment adviser shall ensure that fees charged to the clients is fair and reasonable.

16. From the material available on record, it is noted that SCN and hearing notices sent via digitally signed emails were duly served upon the Noticee No. 2, 5,6, 8 and 9. Further in terms of Rule 7(3) of SEBI Rules, a public notice was published in the newspaper. However, the Noticee neither submitted reply to the SCN nor appeared for the two hearings granted to him. In this regard, I refer to the judgment of Hon’ble Securities Appellate Tribunal (SAT) dated December 08, 2006 in the matter of Classic Credit Ltd. v SEBI (Appeal No. 68 of 2003) wherein, it observed that,

“… the appellants did not file any reply to the second show-cause notice. This being so, it has to be presumed that the charges alleged against them in the show cause notice were admitted by them”.

17. I also observe that the Hon’ble SAT in the matter of Sanjay Kumar Tayal & Ors. v SEBI (Appeal 68 of 2013 dated February 11, 2014) had inter alia observed that,

“… appellants have neither filed reply to show cause notices issued to them nor availed opportunity of personal hearing offered to them in the adjudication proceedings and, therefore, appellants are presumed to have admitted charges leveled against them in the show cause notices…”

18. Before proceeding with allegation-wise submissions of the Noticee No. 1 and 4, preliminary objection of Noticee No. 1 is dealt with. During the hearing Noticee No. 1 submitted that the call recordings of the complainants as provided as an annexure to the SCN cannot be relied upon as it does not satisfy the criteria of section 65-B of the Indian Evidence Act, 1872.

19. In this regard, Hon’ble Supreme Court of India in the matter of Tata Consultancy Services Limited v. Cyrus Investments Pvt. Ltd. (Civil Appeal No. 440-441 of 2020) has observed that:

“… the rigors of CPC and the Evidence Act are not be applicable to Tribunals/Quasi-Judicial Authorities.”

20. The present proceedings before SEBI, are quasi-judicial in nature and hence the Indian Evidence Act shall not apply. Accordingly, section 65B which relates to admissibility of electronic records before a Court of Law, is not applicable to proceedings before SEBI.

21. During the personal hearing, he Authorised Representative of Noticee No. 1 reiterated the same and he was advised to prove that call recording of the complainants relied by SEBI as non-genuine. However, till date he has not brought any material before me in this regard.

22. Now I will proceed to address the allegations as set out in the SCN.

Allegation 1: Noticees Promised Assured / Guaranteed Unrealistic Returns to its Clients

23. It was alleged in the SCN that Noticees had promised assured profit/ target return to their clients (terming them as “approachable profit”) under various pre-defined packages on the investments made by the clients as mentioned below:

Client Name | Payment date | Name of the service | Target Return/ for a profit of (in Rs) | Service Fee (in Rs) Exclusive of GST (18%)** |

Mr. Mohammad Alanoor | 16-01-2018 | Admire Forex Package | 10,60,500 | 3,03,000 |

Routhu Sriramulu Naidu | 22-08-2017 | Radiant Option Package | 6,50,000 | 2,60,000 |

Mr. Sujeet Chandrvar | 05-10-2015 | Bonanza Mcx Platinum | 16,25,000 | 3,25,000 |

Mr. Kelvin Wilson | 04-01-2018 | Crack Future Package | 10,99,000 | 3,14,000 |

Mr. Lakshmi Narain Singh | 27-10-2016 | Tip Top Future Package | 21,76,000 | 5,44,000 |

Jai Prakash Singh | 26-06-2018 | Future Leader Package | 6,50,000 | 2,60,000 |

24. Noicee No. 1 submitted that it had publically displayed the terms and conditions along with its disclaimer and disclosures which were always available to the clients. Even all the investment documents eg. MoUs, payments receipts clearly communicate to the client that the investments are subject to market risks and no assured profits are promised.

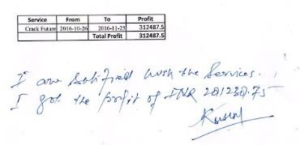

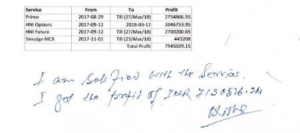

25. The payment receipts submitted by the Noticee No. 1 have been perused and the relevant portion of the payment receipt is reproduced below:

![]()

26. I note from payment receipts issued to the clients and MOU/agreement it entered into with the clients that the Noticees have been promising targeted returns (terming them as “approachable profit”) under various pre-defined packages on the investments made by the clients. Noticee No. 1 has further submitted that target return is clearly mentioned as “it is not guaranteed or assured”.

27. The Noticee No. 1 has submitted that it has never promised or assured any profits to the clients and all clients were aware that investments are subject to market risk. It has submitted that “approachable profits” are basically the profits which can be achieved but are not guaranteed.

If in the case of any client, the “approachable profit” is not generated then the Noticees will provide complimentary services till such time unless the profit generation is done as per the approachable profit.

28. I do not accept this interpretation of the Noticee No. 1 with respect to “approachable profit”. Noticee No. 1 has contended that they do not assure/guarantee an “approachable profit” to its investors; instead they are committing to their clients that they will continue to provide investment advisory services to its clients till such time that the “approachable profit” is achieved. From the plain reading, it appears that the Noticee No. 1 has assured the clients that if he/she continues to act on the investment advice given by Noticee No. 1, he/she will achieve a certain quantifiable return, at sometime or the other. It is observed that on payment receipts, the “approachable profit” has been clearly mentioned against “For a Profit of”. It is a known fact that all investments in the stock market are subject to market risk and a particular return, or for that matter, any form of return on an investment cannot be guaranteed, no matter how long the period for which the investment is held or advice on that investment is offered to the client. I note that the Noticee No. 1, being a registered SEBI intermediary having obtained the necessary certifications, is well aware of this fact and that despite this knowledge has provided such an assurance to its clients.

29. In this regard, it is pertinent to mention the order of Hon’ble Securities Appellate Tribunal (SAT) in the matter of MSS Trading System Centre v. SEBI (Appeal No. 807 of 2022, date of order 12.12.2022) wherein it was provided that:

“We also find that in addition to the aforesaid, the appellant was also giving an assured returns on the investment made by the investors. In this regard, the WTM found that the appellant was offering three types of services and in one of those agreements entered between the appellant and their clients, there was a specific clause for assured / guaranteed returns. We are of the opinion that such assurance of profit given by the appellant was totally fraudulent and in violation of Regulation 4 of the Securities and Exchange Board of India (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003.”

30. Noticee No. 1 has contended that it has been clearly mentioned in the receipts that the targeted return i.e., the “approachable profit” is not guaranteed or assured and the receipts are duly signed by the client. I find that a mere standard statement in the receipt that the “approachable profit” is not guaranteed/assured cannot dilute the conduct of the Noticee No. 1 in making false representation that it can deliver the “approachable profit”. If the Noticee No. 1 know that the investments are subject to market risks, it cannot make any representation that it can deliver any “approachable profit” as mentioned in the payment receipts and complementary service shall be given until approachable profit is achieved. Therefore, it is inferred that Noticee No. 1 made misrepresentation of being capable of delivering the “approachable profit” and therefore violated Regulation 3 (a), (b), (c) and (d), 4(1) and 4(2)(k),(s) of PFUTP Regulations read with Section 12A(a), (b) and (c) of SEBI Act, 1992. Further, from the aforesaid it is inferred that the Noticees have failed to act in a fiduciary capacity towards its clients, thereby violating Regulation 15(1) and Clauses 1 (honesty and fairness) and 2 (diligence) as specified under Third Schedule of Code of Conduct for Investment Adviser read with Regulation 15(9) of IA Regulations

Allegation 2: Selling multiple packages to clients with threat of forfeiture and charged unreasonable and undisclosed fee

31. It was alleged that the Noticees had not been fair in its dealing with their clients by not being transparent about the fee charged to the client and had not been informed of all the charges upfront. It was further alleged that the Noticees had adopted unethical business practices/ modus operandi (promising assured returns, recouping losses, shifting the client to high price package claiming the package is beneficial for the client, etc. Analysis of the fees collected from the clients (sample basis) in the first month of the association with the Noticee No. 1 is tabulated as under:

S. No | Name | Date | No. of product/ package sold | Proposed investment as per Risk Profile | Amount of fees collected |

1. | Mr. Mohammad Alanoor | 29/11/2017 to 29/12/2017 | 03 | 2-5 Lakhs | 3,24,702 |

2. | Routhu Sriramulu Naidu | 22/08/2017 to 20/09/2017 | 04 | 1-2 Lakhs | 7,34,538 |

3. | Mr. Sujeet Chandrvar | 06/07/2015 to 06/08/2015 | 07 | Risk profile not filled. | 8,87,962 |

4. | Ayush Kumar Agrawal | 24/09/2018 to 24/10/2018 | 06 | 5-10 lakhs | 8,33,023 |

5. | Mr. Lakshmi Narain Singh | 23/08/2016 to 26/09/2016 | 04 | 0-1 Lakhs | 1,46,671 |

32. I note that the Noticee No. 1 has not provided any explanation for the charging of huge amount of service fee from clients by allotting multiple packages to in a very short span of time, apart from stating that clients have agreed to make the payments and have opted for such services based upon the reputation and past performance of the Noticee No. 1. The Noticee No. 1 has merely stated that no pressure has been put on the client to make the payment and multiple packages are sold with free consent and full knowledge of the client. Every time a service is sold, a payment receipt is communicated and client signs the same and sends it back to the Noticee No. 1. It has also been submitted that there is no bar in law or any circular issued by SEBI regarding the amount of fees that can be charged by the Noticee No. 1 to the client and that the IA Regulations only expect the IA to charge reasonable fees. Noticee No. 1 have not made any submissions as to how the fee being charged was “reasonable”.

33. As per the prescribed Code of Conduct, investment advisers shall ensure that fees charged to the clients are fair and reasonable. It is observed from the fees charged by Noticee No. 1 to its clients that in couple of instances, Noticee No. 1 has charged the clients more than the proposed investment amount which cannot be termed fair and reasonable even in farfetched possibility. Further, with respect to the allegation of forfeiture of service charge, the copy of the emails provided by Noticee No. 1 appear to be the standard format used across all the clients.

Therefore, it appears that so called “free consent” email was drafted by Noticee No.1 and was made to sign by its clients. I am, therefore, not inclined to accept the submissions made by the Noticee No. 1 in this regard. Therefore, it is inferred that Noticees have violated Regulation 15 (1) of IA regulation and failed to abide by Code of Conduct under Regulation 15(9) of IA Regulations read with clause 1, 2, 5 and 6 of Code of Conduct for Investment Adviser.

Allegation 3 and 4: Whether the Noticee manipulated the risk profiles of clients and hasfailed to conduct due diligence and failed to abide by principles of Suitability

34. The SCN alleged that the Noticees have sold products/services meant for high risk clients to clients who have medium risk It is alleged that the Noticees have sold products/services without considering the clients’ experience, investment objectives and financial situation. Some of the instances are discussed as under:

a. Shahjad Ahmed Khan : In the case of Shahjad Ahmed Khan two risk profile was done by the IA. In one of the risk profile (December 27, 2018- mentioned by the client), it has been noted that the client has very less experience with forex investment unlike other risk profile (January 02, 2019) of the client which provides that client has extensive experience with the forex investment. This shows disparity in the two risk profiles of the same client done within a week time period. Further, from the invoices it is noted that on January 02, 2019 client was sold an ideal Forex package. Thus the IA modifies or manipulate the risk profile of the clients in order to sell the advisory products and maximise its revenue.

b. Jai Prakash Singh : Two risk profiles of Jai Prakash Singh were done. Certain anomalies identified in the two risk profiles of the same client is provided as under:

- Proposed Investment Amount has been changed from less than 1 lakh to 5 – 10 lakhs.

- Gross annual income has been changed from 1-5 lakhs to 5-10 lakhs

- Investment experience has been changed from less than 3 years to more than 5 years.

- Risk tolerance has been changed from medium to high

- Occupation has been changed from Government sector to Private Sector.

c. Kelvin Wilson: The complainant had informed that no Risk profile was created or communicated to him by the Noticees. Further he has informed that he does not hold any Demat account prior to January 03, 2018.

d. Sujeet Sunder Chandavar: The entity has informed that risk profile form provided by the Noticees was filled as per the instructions given by the Company. Further risk profile was done when the client had already paid Rs. 26,900/- to the Noticees.

35. On perusal of the Risk Profiling Questionnaire of Noticee No. 1, it is observed that Risk Profile of Highbrow includes following 02 questions to ascertain risk appetite of the clients:

i. What is your preference w.r.t securities with low risk, low return over high risk, high return?

ii. When market is not performing well do you prefer to buy risky investments and sell less risky investments?

36. In this regard, Noticee No. 1 has submitted that there were 21 questions in the risk profile form, however, SEBI has picked only the two questions. Noticee No.1 submitted that these questions can no manner be called the leading questions.

37. The risk profile provided by Noticee No. 1 has been perused and it is observed that other questions pertain to selection of product. Based on the overall answers to the risk profile form, the suitable product was provided.

38. It is not disputed that at the time of applying for a certificate of registration, a prospective Investment Adviser is required to submit the risk profiling questionnaire. However, the requirement for such a questionnaire is only to ascertain as to whether the prospective Investment Adviser had in place a process for assessing the risk bearing ability of the clients. It was left to the Investment Adviser to frame the risk profiling questionnaire as per the necessary requirements. So, the grant of a certificate of registration cannot be considered as an approval of the questionnaire’s contents or its merits. But I accept the argument of the Noticee that the mention of ‘High Risk’ in the questions were self-explanatory and I find that such questions are the only way to gauge the risk bearing capacity of the clients.

39. Also, the Noticee has submitted that there were a total of 21 questions. Therefore, I find that the aforesaid three questions were not the leading questions. In such a circumstance, the specific allegation made in the SCN that the aforesaid two questions were ambiguous in nature and were the leading questions, is not borne out from the facts.

40. I find that the Noticee’s intent is to first make the client pay towards the service without having any regard for his/her risk appetite. The risk profile is filled by the Noticee in a manner so as to achieve a high risk appetite score and is then sent to the client for his/her signature. The client, having already committed a substantial amount of funds with the Noticee, has no option but to sign on the form and return it to the Noticee or the client stands the risk of forfeiting the money already paid.

41. It was further alleged that the Noticees did not do any financial planning of the client, did not consider client’s investment objective while offering advisory product/services and selling multiple advisory product/services thereby keeping their own interest before the interest of clients. For eg.

L N Singh:

S.No | Date of payment | Name of package | Duration | Target profit | Amount charged |

1. | 23-08-2016 | Options | 3 Months |

| 7250 |

2. | 25-08-2016 | Desire options package | NA | 7,08,000 | 36225 |

3. | 20-09-2016 | Weekly report | 21 report (21 weeks/5 months) |

| 55200 |

4. | 26-29-2016 | Income Future Package |

| 564000 | 47996

|

5. | 23-08-2016 | Options | 3 Months |

| 7250 |

6. | 25-08-2016 | Desire options package | NA | 7,08,000 | 36225 |

7. | 20-09-2016 | Weekly report | 21 report (21 weeks/5 months) |

| 55200 |

8. | 26-29-2016 | Income Future Package |

| 564000 | 47996

|

9. | 29-09-2016 | Income Future Package |

| 564000 | 45000 |

10. | 05-10-2016 | Weekly report | 31 reports (31 weeks/ 7 months) |

| 78550 |

11. | 10-10-2016 | Tip top future package |

| 21,76,000 | 266954 |

12. | 20-10-2016 | Crack Future Package |

| 10,99,000 | 273000 |

13. | 27-10-2016 | Tip top future package |

| 21,76,000 | 352200 |

14. | 27-02-2018 | Bounce Cash Package |

| 10,53,500 | 196000 |

15. | 29-03-2018 | Decisive cash package |

| 6,50,000 | 210001 |

16. | 26-04-2018 | Float Forex Package |

| 6,03,000 | 150000 |

42. The above table provides that 1st service was sold for the tenure of 3 months, but prior to completion of that service 6 more advisory products were sold with profit target. For every new products different target profit is given. Further, on September 20, 2016 weekly report for 21 weeks were sold. Again, just after 15 days, weekly report for 31 weeks were sold. Thus, as per the invoice details, at a given point of time, multiple services were active for the client and no services were fully completed.

43. In this regard, I observe that Noticee No. 1 did not provide the rationale behind the aforementioned arrangement with the complainant Mr. LN Singh. Infact for the proof< Noticee No. 1 only provided the payment receipt dated October 27, 2016 and did not provide any explanation for the transactions prior to that.

44. I find that the objective of suitability assessment is to determine the risk tolerance level of clients and recommend commensurate products/services to the This objective would be defeated if such exercise is not undertaken properly by an investment advisor and would lead to unsuitable and inappropriate services being offered to the clients. From the aforesaid instances, I find that Noticee No. 1 has sole advisory product/service with overlapping subscription period. During such overlap period, the clients shall be receiving duplicate advise/tips/messages and such duplicate tips/advice, if any, is of no use to the clients. This dishonest practice of Noticee No. 1 is completely unprofessional and unethical with a view to enhance service revenue and against the interest of the clients. The material available on record does not show any justification from the Noticees in this regard. The Noticee is seen to have considered the risk profiling and suitability assessment of a client as a mere formality and thus, found to be in non-compliance with the Code of Conduct specified under IA Regulations. Therefore, it is inferred that I am of the opinion that Noticcees have violated regulations 3(a), (b),(c) and (d) of PFUTP Regulations read with section 12A(a),(b) and (c) of SEBI Act, Regulation 15 (1) of IA regulation, and failed to abide by Clause 1 of Code of Conduct for Investment Adviser as mentioned in Schedule III read with regulation 15 (9) and Regulation 17 of IA Regulations.

Allegation V: The Noticees split of fee among the relatives of the client and denied to acknowledge clients even after receiving payment and forcefully captured the card details:

45. It was alleged in the SCN that Noticees were following a practice of obtaining details of relatives of the clients. These relatives were also treated as clients. The payment received from the primary client and services provided is then split among the relatives to show that the Noticees were not charging exorbitant fee from a single client. Some of the instances in which payments have been taken through the family members of the clients are tabulated as under:

S. No | Clients name | Relative’s name | Relationship |

1 | L N singh | Kusum | Wife |

2 | L N singh | Usha | Daughter |

3 | L N singh | Nish | Daughter |

46. It was further alleged that Noticees had used the card of client to take the payments for assigning multiple advisory services.

47. Noticee No. 1 has submitted that it has always treated every client as separate entity and family members opted for the service only after being satisfied the service of Noticee No. 1. Exhibit 63 and 66 submitted by Noticee No. 1 have been perused and it is noted that the same has been claimed by the Noticee No. 1 that the services were rendered to the family members on individual basis and the same was individually acknowledged by the family members as below:

Kusum Singh (wife of LN Singh)

Nisha Singh (daughter of LN Singh)

48. It appears from above that the said acknowledgements are signed by the same person as against the claim of Noticee No. 1. Therefore, I cannot accept the submissions of the Noticee No. 1 that it did not capture the family member details. On the contrary, the aforesaid proves that Noticee No. 1 has not been fair while dealing with its client. Thus, the Noticee No. 1 had not only failed to maintain appropriate standard of conduct but also failed to act in fiduciary capacity to its client and hence, it is inferred that Noticee No. 1 has violated Regulation 15 (1) of IA Regulations and failed to abide by Clauses 1, 2, 5 and 6 of Code of Conduct under Regulation 15 (9) of IA Regulations.

49. Regarding the capturing of card details, Noticee No. 1 has submitted that why such point has not been raised by client post payment and if card details has been forcefully captured, what is the force used by highbrow which made client helpless but to provide his important card details. Also assuming, if card details had been taken, it is the most secure system from RBI that without OTP, Payment cannot be made. OTP Always comes on registered mobile number with the bank. Why Client has provided OTP as well if he did not wish to make payment?

50. Noticee No. 1 has also stated that why the complainant never raised such issue earlier. I am of the opinion that the onus of not sharing the card details also lies with the complainants. When the government, RBI has been making rounds of advertisements in print media/social media then the complainant cannot say that it captured forcefully. In fact, as understood in common parlance, the complainants shared the card details with Noticee No. 1.

Allegation VI: Non redressal of Investor Grievances

51. It was alleged in the SCN that Noticee No 1 did not redress the investor grievances as per the timelines prescribed by SEBI.

52. In this regard, the Noticee No. 1 has submitted that Highbrow has almost submitted the 1st action taken report of almost every complaint with in 7 days highbrow has never delayed in submitting ATR within prescribed time, though the time limit to submit ATR is 30 days. Noticee also states that it has always intended to update & resolve the complaint as mentioned earlier. Highbrow has never been delayed in submission of its action taken report. Out of total complaints pending on scores 29 complaints are resolved as per the email communications received from the client. But in case of long pending complaints it must be noted that complaints were pending either with SEBI officials or with the Investor for very long time.

53. In this regard, the email submitted by Noticee No. 1 has been perused, and it is noted from the email the it refers to only 1 complaint and that doesn’t provide the timelines in which the said complaint was resolved. The said submission of the Noticee No. 1 has no relevance to the fact that there were more than 29 complaints pending with the Noticee No. 1 (provided as annexure 11 to the SCN) and Noticee No. 1 did not provide status of the same and filed ATR thereof. In this context, I would also like to refer to the judgment of the Hon’ble SAT in S. S. Forgings & Engineering Limited & Others v SEBI, (Appeal No. 176 of 2014 decided on August 28, 2014) wherein it, inter alia, observed that

“…This Tribunal has consistently held that redressal of investors’ grievances is extremely important for the Regulator to regulate the capital market. If the grievances are not redressed within a time bound framework, it leads to frustration among the investors’ who may not be motivated to further invest in the capital market.”

54. Therefore, I am of the opinion that Noticee No. 1 has violated SEBI Circular CIR/OIAE/2014 dated December 18, 2014 read with regulation 21(1) (redressal of client grievances) of IA Regulations.

55. With respect to the liability of Noticee Nos. 2-9, I am of the opinion that Noticee Nos. 2-9 being the directors of Noticee No. 1 at the relevant times had a fiduciary duty to comply with the IA Regulations which they failed to do. Noticee No. 1 being the registered company is run by the individuals or directors in the present case. Therefore, Noticee Nos. 2-9 cannot feign ignorance that they had no idea about the way investment advisory has been run by Noticee no. 1. I find that the directors have failed to discharge their duties by acting in the manner as explained in the previous paragraphs and therefore are equally responsible for the aforementioned violations during the tenure of their directorship. It is a settled position of law that in cases of fraud the corporate veil can be lifted and the directors can be held liable for the fraud perpetrated by the corporate entity.

56. Since, Noticee No. 2, 5,6, 8 and 9 have not replies to the SCN, in light of the orders of Hon’ble SAT discussed in paras 16 and 17 of the extant orders, I presume that they have admitted the charges levelled against them in the SCN.

57. Noticcee No. 3 had contended that he was merely in charge of HR and tax matters of Noticee No. 1. However, he has failed to produce any evidence to corroborate the same. In fact Noticee No. 1 in its submission has categorically submitted that submissions of Noticee No. 3 cannot be believed and are denied. On the contrary, it is submitted by the Noticee No. 1 that Noticee No. 3 was involved in the decision making since 2011. As mentioned in pre-paras, the company cannot run by its own. It is the people who run the company and therefore, the directors cannot feign ignorance for the same.

58. Noticee No. 4 submitted that he did not play any active role in the board of the company. In this regard I note that the relationship of the complainants had continued with Noticee No. 1 during the tenure when Noticee No. 4 was a director. In fact, Noticee No. 4 was a director for almost 6 years. Hence, the contention of these directors that they did not exercise control over the management of Highbrow at any point in time and he did not indulge in or facilitate the commissions of the alleged violations is not acceptable.

59. Noticee No. 7 was a director for almost an year. Though Noticee No. 7 has denied the allegations in the SCN but did not bring any evidence which says otherwise.

60. The directors are conferred powers to conduct the business of the company in meeting the objects of the company. Even if the director was only in charge of a specific operational area, the responsibility of the of the board of directors is to exercise all such powers, and to do all such acts and things, as the company is authorized to exercise and do. I am of the opinion that the omission to exercise that power could also lead the liability on the part of the directors.

61. In this regard, I place my reliance on order of Hon’ble Supreme Court (SC) in the matter of Narayanan vs. Adjudicating Officer, SEBI (26.04.2013 – SC) : MANU/SC/0426/2013 wherein Hon’ble SC while dealing with responsibilities/duties/obligations of the directors held the following:

“…The Directors of the company or the person in charge directly or indirectly use or employ, in connection with the issue, purchase or sale of any securities listed in stock exchange, any manipulative or deceptive device or contrivance in contravention of SEBI Act or the Regulations made thereunder have necessarily to be dealt with in accordance with the provisions of the Act and the Regulations which is absolutely necessary for the investor’s protection and to avoid market abuse.

…..

Company though a legal entity cannot act by itself, it can act only through its Directors. They are expected to exercise their power on behalf of the company with utmost care, skill and diligence. This Court while describing what is the duty of a Director of a company held in Official Liquidator v. P.A. Tendolkar MANU/SC/0005/1973 : (1973) 1 SCC 602 that a Director may be shown to be placed and to have been so closely and so long associated personally with the management of the company that he will be deemed to be not merely cognizant of but liable for fraud in the conduct of business of the company even though no specific act of dishonesty is provide against him personally. He cannot shut his eyes to what must be obvious to everyone who examines the affairs of the company even superficially.”

62. Therefore, In the light of the above discussion and the order of Hon’ble SC, conclude that the directors have violated the provisions as enunciated the pre-paras and.

II. Do the violations, if any, on the part of the Noticee attract monetary penalty under Sections 15C, 15EB, 15HA and 15 HB of SEBI Act of SEBI Act?

63. I note that the Hon’ble Supreme Court of India in the matter of SEBI v/s Shri Ram Mutual Fund [2006] 68 SCL 216(SC) held that “In our considered opinion, penalty is attracted as soon as the contravention of the statutory obligation as contemplated by the Act and the Regulations is established and hence the intention of the parties committing such violation becomes wholly irrelevant………. Hence, we are of the view that once the contravention is established, then the penalty has to follow and only the quantum of penalty is discretionary.”

64. In view of the foregoing, I am convinced that the Noticees are liable for monetary penalty under Sections 15C, 15EB, 15HA and 15 HB of SEBI Act for violation of the above mentioned provisions. The provisions of the SEBI Act, 1992 is reproduced as under:

Penalty for failure to redress investors’ grievances

15C. If any listed company or any person who is registered as an intermediary, after having been called upon by the Board in writing including by any means of electronic communication, to redress the grievances of investors, fails to redress such grievances within the time specified by the Board, such company or intermediary shall be liable to a penalty which shall not be less than one lakh rupees but which may extend to one lakh rupees for each day during which such failure continues subject to a maximum of one crore rupees.

Penalty for default in case of investment adviser and research analyst

15EB. Where an investment adviser or a research analyst fails to comply with the regulations made by the Board or directions issued by the Board, such investment adviser or research analyst shall be liable to penalty which shall not be less than one lakh rupees but which may extend to one lakh rupees for each day during which such failure continues subject to a maximum of one crore rupees.

Penalty for fraudulent and unfair trade practices.

15HA.If any person indulges in fraudulent and unfair trade practices relating to securities, he shall be liable to a penalty which shall not be less than five lakh rupees but which may extend to twenty-five crore rupees or three times the amount of profits made out of such practices, whichever is higher

Penalty for contravention where no separate penalty has been provided.

15HB. Whoever fails to comply with any provision of this Act, the rules or the regulations made or directions issued by the Board thereunder for which no separate penalty has been provided, shall be liable to a penalty which shall not be less than one lakh rupees but which may extend to one crore rupees.”

III. If so, what would be the monetary penalty that can be imposed taking into consideration the factors mentioned in Section 15J of SEBI Act, 1992?

65. While determining the quantum of penalty under Section 15A(b) of the SEBI Act, it is important to consider the factors stipulated in Section 15J of the SEBI Act, 1992 read with Rule 5(2) of the Adjudication Rules, 1995 which read as under:

Factors to be taken into account by the adjudicating officer

15J While adjudging quantum of penalty under section 15-I, the adjudicating officer shall have due regard to the following factors, namely

(a)the amount of disproportionate gain or unfair advantage, wherever quantifiable, made as a result of the default;

- the amount of loss caused to an investor or group of investors as a result of the default;

- the repetitive nature of the default.

66. I note that the SCN has not brought out the quantum of profit/gains made by the Noticee No. 1 by way of promising assured returns and charging its clients service fees arbitrarily and collecting unreasonable amount of fees by offering multiple packages. I note that examination report has not brought on record loss caused to the investors due to nonresolution of the complaints. However, violations committed by the Noticee No. 1 are grave and penalty be imposed to commensurate with the said violations.

ORDER

67. Having considered all these facts and circumstances of the case, the material available on record, the factors mentioned in Section 15J of the SEBI Act and in exercise of the powers conferred upon me under Section 15-I of the SEBI Act read with Rule 5 of the SEBI Adjudication Rules, 1995, I hereby impose a penalty of Rs. 5,00,000 (Rupees Five Lakh) on Noticee No. 1 and Rs. 1,00,000 (Rupees One Lakh) each on Noticee Nos. 2-9 for the violations as specified in this order.

68. The said demand draft or forwarding details and confirmations of e-payments made (in the format as given in table below) should be forwarded to “The Division Chief, Enforcement Department (EFD1 –DRA 6), Securities and Exchange Board of India, SEBI Bhavan, Plot C –7, “G” Block, Bandra Kurla Complex, Bandra (E), Mumbai –400 051.

Case Name |

|

Name of the Payee |

|

Date of payment |

|

Amount Paid |

|

Transaction No. |

|

Bank Details |

|

In which payment is made for | Penalty |

69. In the event of failure to pay the said amount of penalty within 45 days of the receipt of this Order, SEBI may initiate consequential actions including but not limited to recovery proceedings under Section 28A of the SEBI Act, 1992 for realization of the said amount of penalty along with interest thereon, inter alia, by attachment and sale of movable and immovable properties.

70. In terms of the provisions of Rule 6 of the Adjudication Rules, copies of this order are being sent to the Noticees, and also to the Securities and Exchange Board of India.

Date : March 31, 2023 SAHIL MALIK

Place : Mumbai CHIEF GENERAL MANAGER &

ADJUDICATING OFFICER