QJA/AA/MIRSD/MIRSD-SEC-2/29989/2023-24

SECURITIES AND EXCHANGE BOARD OF INDIA

ORDER

UNDER SECTION 12(3) OF SECURITIES AND EXCHANGE BOARD OF INDIA ACT,

1992 READ WITH REGULATION 27 OF SECURITIES AND EXCHANGE BOARD OF INDIA (INTERMEDIARIES) REGULATIONS, 2008

In respect of –

Equity99 (PAN – AAFFE4984L)

[SEBI Registration No. INA000005358]

In the matter of non-compliance by Investment Advisor – Equity 99

BACKGROUND:

1. Securities and Exchange Board of India (hereinafter referred to as “SEBI“) had conducted an inspection of Equity99 (hereinafter referred to as “Noticee”/ “Equity99”), a SEBI registered Investment Advisor having Registration No. INA000005358 for the period April 01, 2021 to August 31, 2022 (hereinafter referred to as “inspection period”). Thereafter, the findings of the said inspection were communicated to the Noticee, vide email dated November 09, 2022. In response to the findings of the inspection report, the Noticee, vide letter dated November 14, 2022, had submitted its reply to SEBI.

2. Based on the response received from the Noticee, a post inspection analysis was prepared and the following alleged violations of the provisions of SEBI (Investment Advisers) Regulations, 2013 (IA Regulations, 2013), SEBI (Research Analysts) Regulations, 2014 (RA Regulations, 2014) and various SEBI Circulars issued thereunder were observed:

A. Qualification and Certification Requirements: Principal Officer of Equity 99 did not have valid NISM Certificate during the inspection period thereby allegedly violating the provisions of Regulation 15(13) read with Regulation 7(2) of the IA Regulations, 2013.

B. Condition of certificate: Equity99 has not included word Investment Advisor in its name thereby allegedly violating the provisions of Regulation 13(a)(c) of the IA Regulations, 2013 read with Clause 8 & 9 of the Code of Conduct as specified in Third Schedule of IA Regulations, 2013.

C. Format of Agreement: Equity99 has been collecting fees and rendering advice to the clients prior to execution of the agreement with its clients thereby allegedly violating the provisions of Regulation 19 (1) (d) of the IA Regulations, 2013 read with Clause (ii) c of SEBI circular SEBI/HO/IMD/DF1/CIR/P/2020/182 dated September 23, 2020.

D. General Responsibility: Equity 99 has sold the research report to its telegram channel clients, by not obtaining a certificate of registration of Research Analyst from SEBI thereby allegedly violating the provisions of Regulation 15(9) of the IA Regulations, 2013 read with Clause 1, 2, 5, 8 & 9 of Code of Conduct as specified in Third Schedule of IA Regulations, 2013 and Regulation 3 (1) of the RA Regulations, 2014.

E. Risk Profiling: Risk profiling of clients has not been done properly, appropriate category of risk and risk profiling scores has not been communicated to clients thereby allegedly violating the provisions of Regulation 16 (b) (iii) & 16 (e) of IA Regulations, 2013.

F. Suitability: Equity99 has recommended same service to clients falling under Low, Medium & High risk categories. Thus, Equity99 failed to maintain appropriate standards of conduct and failed to act honestly, fairly and in the best interests of its clients and in the integrity of the market thereby allegedly violating the provisions of Regulation 17 (a), (c) and (d) read with Clause 1 and 9 of Code of Conduct under Regulations 15(9) of IA Regulations, 2013.

G. Redressal of client grievances: One Complaint of Mr. Arun Joshi is still pending to be resolved by Equity 99 in SCORES thereby failing to redress client grievance promptly in violation of Regulation 21 (1) and (2) of the IA Regulations, 2013.

I. Know your Client procedures: Equity99 has not followed know your client (KYC) procedure properly and on-boarding the clients without verifying that Client is KYC Compliant or not with any KRA (KYC registration Agency) thereby allegedly violating the provisions of Regulation 15(8) of IA Regulations, 2013.

J. Display of Mandatory Information: Equity 99 has displayed incorrect details of investor complaints in the trend of annual disposal of complaints on its website thereby allegedly violating the provisions of Clause 2 of SEBI Circular CIR/MIRSD/3/2014 dated August 28, 2014 and Regulation 15(9) of the IA Regulations, 2013 read with Clause 8 of Code of Conduct as specified in Third Schedule of IA Regulations, 2013.

ENQUIRY PROCEEDINGS BY DESIGNATED AUTHORITY

3. In view of the same, SEBI initiated enquiry proceedings under Regulation 23 of the Securities and Exchange Board of India (Intermediaries) Regulations, 2008 (‘Intermediaries Regulations, 2008’) read with Section 12(3) of the SEBI Act, 1992. Vide communiqué dated August 04, 2023, Designated Authority (‘DA’) was appointed under Regulation 24 of the Intermediaries Regulations, 2008 to enquire and make recommendations under Regulation 25 and 26 of the Intermediaries Regulations, 2008 in respect of the alleged violations of the abovementioned provisions of law by the Noticee. Accordingly, in terms of Regulation 25(1) of the Intermediaries Regulations, 2008, the DA issued an Enquiry Show Cause Notice dated September 26, 2023 (hereinafter referred to as the Enquiry SCN) to the Noticee to show cause as to why appropriate recommendations be not made for the alleged violations as mentioned above. The Enquiry SCN was issued to the Noticee by Speed Post Acknowledgement Due (SPAD) at the last known correspondence address “A wing, 912, Dalamal Tower, 9th Floor, Free Press Journal Marg, Nariman Point, Mumbai – 400021” and also via email address [email protected]. Vide email dated November 03, 2023, one Mr. Rahul Sharma, Principal Officer of Equity99 had filed a reply to the SCN via email id [email protected] and thereafter, had attended personal hearing before the DA on November 06, 2023.

4. Thereafter, upon completion of the enquiry, an Enquiry Report dated November 29, 2023 (“Enquiry Report”) was submitted by the DA to the Competent Authority having the following recommendation:

“In view of the violations as established, facts and circumstances of the case, I recommend that regulatory censure be issued against Noticee as specified under Regulation 26(1)(vii) of the Intermediaries Regulations read with Regulation 28 of IA Regulations and Section 12(3) of SEBI Act in the instant enquiry proceeding initiated vide SCN dated September 26, 2023. Therefore, in terms of aforesaid Regulations, I recommend the issuance of regulatory censure against Noticee, i.e., Equity99 [Registration No. INA000005358].”

POST ENQUIRY PROCEEDINGS BY COMPETENT AUTHORITY

SHOW CAUSE NOTICE, REPLY AND PERSONAL HEARING

5. A post-enquiry Show Cause Notice dated December 14, 2023 (hereinafter referred to as “Post Enquiry SCN”) was issued to the Noticee enclosing therewith a copy of the Enquiry Report submitted by the DA and calling upon it to show cause in terms of Regulation 27 of the Intermediaries Regulations, 2008 as to why action as recommended by the DA or any other action as contemplated under the said provision of the Intermediaries Regulations, 2008 should not be taken against the Noticee for the non-compliances / violations of the provisions of law. The said post enquiry SCN was issued via SPAD and via email at id [email protected]. Vide email dated December 20, 2023, Mr. Rahul Sharma, Partner and Principal Officer of Equity99, acknowledged receipt of the SCN and stated that he would be filing a reply to the said SCN within timelines. Thereafter, vide email dated December 25, 2023, the Noticee filed a reply dated December 24, 2023 to the post enquiry SCN and made the following submissions:

(i) The Noticee submits taking note of the observations of the DA as specified under the Enquiry Report dated November 29, 2023 very seriously. In view of the said observations, the Noticee is conducting an immediate review of all respective practices and also enhancing the internal controls to prevent recurrence of such instances.

(ii) The Noticee assures its unwavering commitment to compliance with all regulatory requirements. The Noticee further states that with corrective measures it is implementing, such issues will not recur in the future.

6. Thereafter, in the interest of natural justice, an opportunity of personal hearing was granted to the Noticee on January 09, 2024 vide hearing notice dated December 28, 2023. On scheduled date, Mr. Rahul Sharma, Partner and Principal Officer of the Noticee attended the hearing on behalf of Equity99 through webex and reiterated the submissions made in the reply dated December 24, 2023.

CONSIDERATION OF ISSUES AND FINDINGS

7. I have carefully examined the allegations made against the Noticee and the replies filed to the Enquiry SCN and the post enquiry SCN and the documents / material available on record. The issues that arise for consideration in the instant case is to examine whether the Noticee has violated the provisions of the IA Regulations, 2013, RA Regulations, 2014 along with the SEBI circulars as alleged in paragraph no. 2 above and whether the recommendations made by the DA in the Enquiry Report may be issued in respect of the Noticee. Further, the submissions made by the Noticee to the enquiry SCN are being dealt in detail at the time of dealing with the issues at length at the subsequent paragraphs.

8. Before moving forward, I find it apposite to refer to the relevant provisions of the IA Regulations, 2013, RA Regulations, 2014 along with the SEBI circulars alleged to be violated by the Noticee and the relevant provision of the Intermediaries Regulations, 2008, which are reproduced as under:

IA Regulations, 2013:

Qualification and certification requirement.

7.(2) An individual investment adviser or principal officer of a non-individual investment adviser, registered under these regulations and persons associated with investment advice shall have, at all times a certification on financial planning or fund or asset or portfolio management or investment advisory services-

- from NISM; or

- from any other organization or institution including Financial Planning Standards Board of India or any recognized stock exchange in India provided such certification is accredited by NISM:

Provided that fresh certification must be obtained before expiry of the validity of the existing certification to ensure continuity in compliance with certification requirements:

Provided further that fresh certification before expiry of the validity of the existing certification shall not be obtained through a CPE program.

Conditions of certificate.

13. The certificate granted under regulation 9 shall, inter alia, be subject to the following conditions:-

(a) the investment adviser shall abide by the provisions of the Act and these regulations;

(b)………

(c) the investment adviser, not being an individual, shall include the words ‘investment adviser’ in its name:

Provided that if the investment advisory service is being provided by a separately identifiable department or division or a subsidiary, then such separately identifiable department or division or subsidiary shall include the words ‘investment adviser’ in its name;

General responsibility.

15.(8) An investment advisor shall follow Know Your Client procedure as specified by the Board from time to time.

(9) An investment adviser shall abide by Code of Conduct as specified in Third Schedule.

(13) It shall be the responsibility of the investment adviser to ensure compliance with the certification and qualification requirements as specified under Regulation 7 at all times.

Risk profiling.

16. Investment adviser shall ensure that,-

(b)it has a process for assessing the risk a client is willing and able to take, including:

(i)assessing a client’s capacity for absorbing loss;

(ii)identifying whether client is unwilling or unable to accept the risk of loss of capital;

(iii)appropriately interpreting client responses to questions and not attributing inappropriate weight to certain answers.

Suitability.

17. Investment adviser shall ensure that,-

(a) All investments on which investment advice is provided is appropriate to the risk profile of the client;

(b)………

(c) It understands the nature and risks of products or assets selected for clients;

(d) It has a reasonable basis for believing that a recommendation or transaction entered into:

(i) meets the client’s investment objectives;

(ii)is such that the client is able to bear any related investment risks consistent with its investment objectives and risk tolerance;

(iii) is such that the client has the necessary experience and knowledge to understand the risks involved in the transaction.

Maintenance of records.

19.(1) An investment adviser shall maintain the following records,-

(a)……….

(b)………

(c)………

(d) Copies of agreements with clients, incorporating the terms and conditions as may be specified by the Board;

(e)………

Redressal of client grievances.

21.(1) The Investment Adviser shall redress investor grievances promptly but not later than twenty-one calendar days from the date of receipt of the grievance and in such manner as may be specified by the Board.

(2) An investment adviser shall have adequate procedure for expeditious grievance redressal.

THIRD SCHEDULE

Securities and Exchange Board of India (Investment Advisers) Regulations, 2013 [See sub-regulation (9) of regulation 15]

1. Honesty and fairness.

An investment adviser shall act honestly, fairly and in the best interests of its clients and in the integrity of the market.

2. Diligence

An investment adviser shall act with due skill, care and diligence in the best interests of its clients and shall ensure that its advice is offered after thorough analysis and taking into account available alternatives.

5. Information to its clients

An investment adviser shall make adequate disclosures of relevant material information while dealing with its clients.

8. Compliance

An investment adviser including its partners, principal officer and persons associated with investment advice shall comply with all regulatory requirements applicable to the conduct of its business activities so as to promote the best interests of clients and the integrity of the market.

9. Responsibility of senior management

The senior management of a body corporate which is registered as investment adviser shall bear primary responsibility for ensuring the maintenance of appropriate standards of conduct and adherence to proper procedures by the body corporate.

RA Regulations, 2014

Application for grant of certificate.

3.(1) On and from the commencement of these regulations, no person shall act as a research analyst or research entity or hold itself out as a research analyst unless he has obtained a certificate of registration from the Board under these regulations: Provided that any person acting as research analyst or research entity before the commencement of these regulations may continue to do so for a period of six months from such commencement or, if it has made an application for a certificate of registration under sub-regulation (2) within the said period of six months, till the disposal of such application:

Provided further that an investment adviser, credit rating agency, asset management company or fund manager, who issues research report or circulates/distributes research report to public or its director or employee who makes public appearance, shall not be required to seek registration under regulation 3, subject to compliance of Chapter III of these regulations.

SEBI Circular No. SEBI/HO/IMD/DF1/CIR/P/2020/182 dated September 23, 2020. Guidelines for Investment Advisers

1. Securities and Exchange Board of India (SEBI), after considering the inputs from public consultation, reviewed the framework for regulation of Investment Advisers (IA) and notified Securities and Exchange Board of India (Investment Advisers) (Amendment) Regulations, 2020 (hereinafter referred as “amended IA Regulations”) on July 03, 2020. These amendments shall come into force on September 30, 2020.

2. In addition to the above, Investment Advisers shall ensure compliance with the following guidelines:

(i) Regulation 19 (1) (d) of the amended IA Regulations provides that IA shall enter into an investment advisory agreement with its clients. The said agreement shall mandatorily cover the terms and conditions provided in Annexure-A.

(ii) Agreement between IA and the client

a……..

b…….

c. IA shall ensure that neither any investment advice is rendered nor any fee is charged until the client has signed the aforesaid agreement and provided copy of signed agreement to the client.

SEBI Circular No. CIR/MIRSD/3/2014 dated August 28, 2014.

Information regarding Grievance Redressal Mechanism

1. SEBI has been taking various measures to create awareness among investors about grievance mechanisms available to them through workshops as well as through print and electronic media.

2. As an additional measure and for information of all investors who deal/ invest/ transact in the market, it has now been decided that offices of all Stock Brokers (its registered Sub-Broker(s) and Authorized Person(s)) and Depository Participants shall prominently display basic information, as provided in AnnexureA, about the grievance redressal mechanism available to investors. For other intermediaries, the information as provided in Annexure-B shall be prominently displayed in their offices.

SEBI Circular No. SEBI/HO/IMD/IMD-II CIS/P/CIR/2021/0686 dated December 13, 2021

Publishing Investor Charter and disclosure of Investor Complaints by Investment Advisers on their websites/ mobile applications

3. Further, SEBI issued Circular No. SEBI/HO/IMD/DF1/CIR/P/2019/169 dated December 27, 2019 which inter alia at Para 1 (iv) prescribed display of complaints status by Investment Advisers (IAs) on respective websites/mobile application. In order to further enhance transparency in grievance redressal, the Investment Advisers shall disclose the details of investor complaints by 7th of the succeeding month in the revised format as per Annexure –B on a monthly basis. The para 1 (iv) of the aforesaid circular stands modified accordingly. Investment Advisers not having websites/mobile applications shall send status of Investor Complaints to the investors on their registered email on a monthly basis in compliance of this circular.

9. Now, I would be dealing with each of the alleged violations by the Noticee in detail.

Qualification and Certification Requirements Allegation No. 1:

9.1 Upon inspection, it was noticed that National Institute of Securities Markets (NISM) certificate of Mr. Rahul Sharma had expired on April 01, 2022. Mr. Rahul Sharma was the principal officer of Equity 99 and was providing investment advice during the inspection period without having valid NISM certificate. In view of the same, it was alleged that the Noticee has violated the provisions of Regulation 15(13) read with Regulation 7(2) of the IA Regulations, 2013.

Submissions and Findings:

9.2 I note that in the reply to the post enquiry SCN, the Noticee has not made any specific submission with respect to the said allegation. However, I note from the Enquiry Report and the documents available on record that in the reply filed by the Noticee to the enquiry SCN, the Noticee has admitted that Mr. Rahul Sharma (Principal Officer of Equity99) had failed to renew the relevant NISM certificate which had expired on April 01, 2022 and the details of the same are as under:

Principal officer of Equity 99 | Certification | Certificate validity | |

Rahul Sharma | Investment Advisor Level- 1 | 08/07/2017 | 01/04/2022 |

Investment Advisor Level- 1 | 09/12/2017 | 01/04/2022 | |

9.3 I note that in terms of Regulation 15(13) of IA Regulations, 2013, an Investment Advisor is under an obligation to comply with the certification and qualification requirements as specified under Regulation 7 at all times. In terms of Regulation 7(2) of IA Regulations, 2013, the Investment Adviser is under an obligation, to have at all times, a certification on financial planning or fund or asset or portfolio management or investment advisory services- (a) from NISM; or (b) from any other organization or institution including Financial Planning Standards Board of India or any recognized stock exchange in India provided such certification is accredited by NISM.

9.4 I further note that in the said reply before the DA, the Noticee had claimed that it had taken corrective action promptly by not on-boarding any new clients. In terms of the provisions of Regulation 15(13) read with Regulation 7(2) of the IA Regulations, 2013, Mr. Rahul Sharma, being the principal officer of Equity99 giving investment advice during the inspection period, was under a statutory obligation to have a valid certificate to continue giving Investment Advice to its clients. Considering that the NISM certification of Mr. Rahul Sharma continues to stand expired for around 20 months (expired on April 01, 2022) and the fact that the Noticee has not brought on record any documentary evidence showing steps taken towards renewal of the said certification, I am constrained to conclude and agree with the findings of the DA in the Enquiry Report dated November 29, 2023 that the Noticee, by failing to renew and have a valid certification for continuing as a SEBI registered investment advisor until now, is in violation of the provisions of Regulation 15(13) read with Regulation 7(2) of the IA Regulations, 2013.

B. Condition of certificate Allegation No. 2:

9.5 During the inspection, it was observed that the Noticee had not included the word “Investment Advisor” in its name which is in violation of the provisions of Regulation 13(a) and (c) of the IA Regulation, 2013 read with Clauses 8 and 9 of the Code of Conduct as specified in the Third Schedule of the IA Regulations, 2013.

Submissions and Findings:

9.6 The Noticee, vide its reply dated November 03, 2023 to the enquiry SCN, had submitted that Equity99 is registered with SEBI as an investment adviser in the form of Partnership firm. The Noticee has established a structured framework to ensure the effective segregation of functions and responsibilities within the organization. Its aim is to maintain strict compliance with SEBI regulations while delivering quality investment advisory services to its clients. Therefore, the Noticee stated that it has divided its operations into separately identifiable divisions named as ‘Investment Advisory’ Division, ‘Compliance’ Division and’ Administrative’ Division. Further, it is the case of the Noticee that at the time of submitting its application for registration as an Investment Adviser (IA), the name “Equity99” was provided to SEBI as part of the application process. During the review of its application, no contentions or observations were raised by SEBI regarding its name. The Noticee states that its IA registration application was approved by SEBI without any reservations or objections.

9.7 I note that Regulation 13 of the IA Regulations specifies conditions of certificate granted under Regulation 9 of the IA Regulations, 2013. I note that in terms of Regulation 13(a) of the IA Regulations, 2013 the certificate of registration granted under Regulation 9 of the said Regulations are subject to the condition that the Investment Adviser shall abide by the provisions of the SEBI Act, 1992 and the IA Regulations, 2013. Further, Regulation 13(c) of the IA Regulations, 2013 specifically states that the Investment Adviser, not being an individual, shall include the words ‘investment adviser’ in its name. However, the proviso to the said provision clarifies that if the investment advisory service is being provided by a separately identifiable department or division or a subsidiary, then such separately identifiable department or division or subsidiary shall include the words ‘investment adviser’ in its name.

9.8 Considering that the Noticee is a Partnership Firm, i.e. not being an individual, providing Investment Advisory Services having registration with SEBI, the Noticee was under a statutory obligation to abide by all the provisions of the IA Regulations, 2013 which specifically state that the words “Investment Adviser” have to be included in the name of the registered Investment Adviser. In view of the same, the aforementioned submission of the Noticee cannot be accepted.

9.9 Further, the Noticee has stated that at the time of submitting its application for registration as an Investment Adviser (IA), the name “Equity99” was provided to SEBI as part of the application process and during the review of its application, no contentions or observations were raised by SEBI regarding its name. Here, it is pertinent to mention that Form A in the First Schedule to the IA Regulations, 2013 is the format of the Application for grant of certificate of registration. Further, Form B in the First Schedule to the IA Regulations, 2013 is the format of the Certificate of registration as investment adviser. The said form specifically states that the said registration is subject to the conditions specified in the SEBI Act, 1992 and in the regulations made thereunder. Therefore, the onus of abiding by the provisions of the SEBI Act, 1992 and IA Regulations, 2013 is on the Noticee, it being a SEBI registered intermediary which it has failed to comply with. In view of the same, I find that the Noticee, by not complying with the condition of registration, has violated Regulation 13(a) and (c) of the IA Regulations, 2013.

C. Format of Agreement Allegation No. 3:

9.10 During inspection, it was observed that the Noticee had collected money from two clients viz. Mr. Arun Joshi and Mr. Nikhil Jawahire, while their agreement / KYC was yet to be completed. Thus, it is observed from the process followed by the Noticee that the clients had paid the fees to the Noticee first and then all the formalities of agreement / KYC were completed. In view of the same, it is alleged that the Noticee has violated the provisions of Regulation 19(1)(d) of the IA Regulations read with Clause (ii)(c) of the SEBI Circular No. SEBI/HO/IMD/DF1/CIR/P/2020/182 dated September 23, 2020.

Submissions and Findings:

9.11 I find that no specific submissions have been made by the Noticee with respect to the specific allegations / findings in the Enquiry Report. However, I note the Noticee had made certain submissions for the said allegation before the DA which are reproduced below:

“As a standard practice, our clients were not provided with advisory services prior to fee collection, execution of agreements, and risk profiling. This deviation from standard practice occurred inadvertently in two cases due to a misunderstanding on the part of our onboarding staff. The same has been validated by the inspecting team as well. In light of these lapses, we have taken immediate corrective measures to prevent any recurrence. We have introduced a “maker and checker” concept in our process, ensuring that advisory services are not delivered to clients before all necessary compliance requirements are met. We are committed to upholding the highest standards of professionalism and compliance, and we consider this process enhancement a crucial step in that direction. We would like to emphasize that these lapses occurred in only two out of the many client onboarding processes we manage. While this is no excuse for any oversight, we want to assure you that our commitment to the highest levels of service remains unchanged. We want to highlight the fact that these lapses were not intentional practices adopted by our organization but rather inadvertent occurrences, stemming from misunderstandings on the part of our onboarding staff and we have taken corrective steps to rectify the situation and ensure that such incidents do not repeat in the future. We want to assure you that these isolated occurrences do not reflect our standard practice for client servicing”.

9.12 I find that Regulation 19(1)(d) of the IA Regulations, 2013 specifies that the Investment Adviser shall enter into an investment advisory agreement with its clients. Further, SEBI Circular No. SEBI/HO/IMD/DF1/CIR/P/2020/182 dated September 23, 2020, inter alia, specifies that the said agreement shall mandatorily cover the terms and conditions provided in Annexure A of the said Circular. Annexure A to the SEBI Circular dated September 23, 2020 specifies as under:

“Investment Advisor shall ensure that the following terms and conditions are incorporated in the Investment Advisory Agreement:

1…………..

2. The agreement shall clearly provide for in the first page:

(a) the consent of the client on the following understanding:

- “I / We have read and understood the terms and conditions of Investment Advisory services provided by the Investment Adviser along with the fee structure and mechanism for charging and payment of fee.

- Based on our written request to the Investment Adviser, an opportunity was provided by the Investment Adviser to ask questions and interact with ‘person(s) associated with the investment advice’”. (b) Declaration from the Investment Adviser that:

- Investment Adviser shall neither render any investment advice nor charge any fee until the client has signed this agreement.

- Investment Adviser shall not manage funds and securities on behalf of the client and that it shall only receive such sums of monies from the client as are necessary to discharge the client’s liability towards fees owed to the Investment Adviser.

- Investment Adviser shall not, in the course of performing its services to the client, hold out any investment advice implying any assured returns or minimum returns or target return or percentage accuracy or service provision till achievement of target returns or any other nomenclature that gives the impression to the client that the investment advice is risk-free and/or not susceptible to market risks and or that it can generate returns with any level of assurance.”

9.13 From the above, it is clear that the Investment Advisor is under an obligation to follow the procedure of entering into an agreement with its clients in terms of the provisions mentioned under the IA Regulations, 2013. I find that Clause 2(ii)(c) of SEBI/HO/IMD/DF1/CIR/P/2020/182 dated September 23, 2020 clearly prohibits an investment advisor to render any investment advice or charge any fee until the client has signed the agreement and a copy of signed agreement is given to the client. Further, Annexure A to the SEBI Circular dated September 23, 2020 specifically states that Investment Adviser shall neither render any investment advice nor charge any fee until the client has signed this agreement. However, in the instant case, it is noted that the Noticee had charged fees and rendered services to two of its clients before even entering into an agreement with them. I note from the submissions of the Noticee that it has admitted that there was a deviation from the standard practice which occurred inadvertently in two cases due to a misunderstanding on the part of its onboarding staff.

9.14 In view of the admission on the part of the Noticee with respect to the said charge, I conclude and agree with the findings of the DA in the Enquiry Report dated November 29, 2023 that the Noticee, by failing to enter into an agreement with two of its clients before providing them investment advisory services and charging fees from them, has violated the provisions of Regulation 19 (1) (d) of the IA Regulations, 2013 read with Clause 2(ii)(c) of SEBI Circular No. SEBI/HO/IMD/DF1/CIR/P/2020/182 dated September 23, 2020.

D. General Responsibility Allegation No. 4:

9.15 During inspection. It was observed that the website of Equity99 has a tab “Research Report” which, inter alia, mentions as under:

“Professional Research

Our Professional Research Analysts are well qualified in each key area of Technical and Fundamental Research with extensive experience in equity analysis. When it comes to investment, fundamental and technical analysis as well as research is highly important.”

9.16 Further, it mentions that “following all due-diligence and compliance procedure as per SEBI regulations and run by team of qualified CAs and CFAs(US) with rich experience in investment analysis and portfolio management”. In view of the same, SEBI had sought certain clarifications from the Noticee during the inspection. In reply to the clarification sought by SEBI regarding the team members having CA and CFA (US) qualification, vide letter dated September 29, 2022, the Noticee had submitted that ““Thank you for pointing out, Equity99 had 2 employees earlier back in 2018 so at that time the website was updated mentioning CA/CFA. Now we have updated the Page & have corrected the same, Kindly Check updated page now https://www.equity99.com/equity–research”. In view of the same, it was observed that the Noticee had displayed incorrect information of preparation of research report by professional research analysts and having CA and CFA(US) as team members on its website.

9.17 Further, it was also observed that the Noticee had sold research report to individuals without having registration of a Research Analyst and without making disclosures in this regard to the individuals to whom the research report was sold. Vide email dated October 13, 2022 to SEBI, the Noticee confirmed that during the inspection period, it had sold Research Reports to individuals (who are not clients but are members of telegram channel of IA-Equity99) for Rs. 46,67,427/-. The research reports were also provided complimentary, as part of HNI membership, to existing clients. Hence, it was observed that as Noticee was selling the research reports and earning consideration from it, this transaction cannot be categorized as “issuing research report to public”. In view of aforesaid, it was observed that Noticee sold research report to its clients without obtaining SEBI Research Analyst registration. Thus, it was alleged that the Noticee has violated the provisions of Regulation 15(9) of the IA Regulations, 2013 read with Clauses 1, 2, 5, 8 & 9 of the Code of Conduct as specified in Third Schedule of the IA Regulations, 2013 and Regulation 3(1) of the RA Regulations, 2014.

Submissions and Findings:

9.18 The Noticee had made the following submissions before the DA regarding the said charge:

“In accordance with the SEBI (Research Analysts) Regulations, we note the following provision:

“3. (1) On and from the commencement of these regulations, no person shall act as a research analyst or research entity or hold itself out as a research analyst unless he has obtained a certificate of registration from the Board under these regulations:

Provided that any person acting as research analyst or research entity before the commencement of these regulations may continue to do so for a period of six months from such commencement or, if it has made an application for a certificate of registration under sub-regulation (2) within the said period of six months, till the disposal of such application:

Provided further that an investment adviser, credit rating agency, asset management company, or fund manager, who issues a research report or circulates/distributes a research report to the public or its director or employee who makes a public appearance, shall not be required to seek registration under regulation 3, subject to compliance with Chapter III of these regulations.”(emphasis supplied)

Based on our interpretation of the regulations, an Investment Adviser (IA) is permitted to distribute research reports to the public for a fee without the necessity of obtaining a Research Analyst Registration. The distribution process includes the provision of services on a chargeable basis. As a result, we provide our research reports to the public. This distribution is facilitated through our public Telegram channel, which is open for the public to join.

Our Telegram channel serves as a platform to communicate our research report offerings to the public, and interested individuals voluntarily subscribe to access our research reports.

In SEBI order WTM/SKM/54/201-22 dated January 12, 2022, by Hon’ble Whole Time Member Shri S. K. Mohanty, the Whole Time Member had observed that- As part of its many novel features, Telegram allows creation of public channels wherein large number of subscribers can be added to be part of it……………….

In view of the above, distribution of reports to telegram subscribers are nothing but distribution of reports to public, which is specifically allowed as per the regulation mentioned above.”

9.19 With respect to the allegation of displaying incorrect information on the Noticee’s website pertaining to the qualification of its team members being CA and CFA (US), I find that the Noticee has admitted that it had not updated its website and that it had two employees back in the year 2018 with the said qualification. As the Noticee does not have employees with the said qualification currently, the Noticee has clarified that it has now updated its website in this regard.

9.20 With respect to the allegation of distributing research paper without obtaining a certificate of registration as a Research Analyst, I note that the Noticee has, in its reply, stated that distribution of research report is facilitated through its public Telegram channel, which is open for the public to join. Further, the Noticee has also stated that its Telegram channel serves as a platform to communicate its research report offerings to the public and interested individuals voluntarily subscribe to access our research reports on payment of fees. Therefore, it is clear that the research reports are available only to the subscribers of the Telegram channel on payment of fees and not to the public at large. I note that in terms of the proviso to Regulation 3(1) of the RA Regulations, 2014, an investment adviser, credit rating agency, asset management company, or fund manager, who issues a research report or circulates / distributes a research report to the public or its director or employee who makes a public appearance, shall not be required to seek registration under regulation 3, subject to compliance with Chapter III of these regulations. Thus, the said proviso clearly exempts an Investment Advisor from the requirement of obtaining a certificate of registration as a research analyst if, the said intermediary is distributing a research report to public. In the instant case in hand, I find that although the research reports were being advertised on the Noticee’s Telegram Channel, the said research reports were made available by the Noticee only to the subscribers of the said Telegram Channel; that too upon payment of fees. Therefore, the submission of the Noticee that it was distributing / circulating the research reports to the public at large which did not require any registration as a Research Analyst is not tenable. I note that the application Telegram is essentially an application based Chat platform. As part of its many novel features, Telegram allows creation of public channels wherein large number of subscribers can be added to be part of it, without disclosing the identity of the persons behind such channel. Such a Channel essentially acts as a message dissemination forum where the Administrators only are allowed to disseminate messages, the content of which is solely decided by them. The subscribers, on the other hand, can only read / view such content and such subscribers do not have any option to send messages or respond to the messages sent by the Administrators. However, in the instant case, the Noticee was not only distributing the research reports on its Telegram Channel to a specific group of subscribers but was distributing the same for consideration i.e. upon payment of fees. Also, the Noticee has, during the inspection period, confirmed that it had sold Research Reports to individuals (who are not clients but are members of telegram channel of Equity99) for Rs. 46,67,427/-.

9.21 In view of the above, I agree with the findings of the DA in the Enquiry Report dated November 29, 2023 that the Noticee, by displaying incorrect information on its website and also, by distributing research reports to specific persons i.e. the subscribers of its Telegram Channel for consideration, is in violation of the provisions of Regulation 15(9) of IA Regulations, 2013 read with Clauses 1, 2, 5, 8 and 9 of the Code of Conduct as specified in Third Schedule of IA Regulations, 2013 and Regulation 3(1) of RA Regulations, 2014.

E. Risk Profiling and Suitability Allegation Nos. 5 and 6:

9.22 As per the submission of the Noticee for Post Inspection Questionnaire (“PIQ”), Risk profiling assessment was done by the Noticee using Risk profiling questionnaire, based on which risk score of the client is determined and depending on the risk score, client risk tolerance was categorized as ‘Low’, ‘moderate’ or ‘High’ which was communicated to the clients over email as per Noticee. Further, based on the risk profile assessment, suitability assessment was done and services were offered to the client based on their risk profile. On perusal of the submission of Noticee for PIQ, it was observed that there are 7 (seven) questions in the Risk Profile Questionnaire framed by the Noticee for its clients. Through the risk profiling questionnaire, the Noticee obtains information such as age, income details, liability / borrowing details, existing investment details, investment objective including the time for which the client wish to stay invested, purpose of investment etc. The risk profiling questionnaire also has questions to assess clients’ willingness to accept the risk of loss of capital.

9.23 From the risk profiling Questionnaire Analysis Process document provided by Noticee, it was observed that the clients would come under any of the following three categories after their risk profiling is carried out by it:

- Low risk category client: Scoring less than 9.

- Medium risk category client: Scoring between 9 to 14.

- High risk category client: Scoring more than 14 to 21.

9.24 On examination of risk profiling questionnaire filled up by few of the clients, it was observed that even if a client had scored less than or equal to 14, it had been categorized under High risk client. Therefore, it was observed that the risk profiling of clients was not done properly by the Noticee. Further, as per its “risk profiling Questionnaire Analysis process”, risk profiling is done twice i.e. once before offering a free trial and then again at the time of service subscription. However, no such documents were produced during inspection, which could prove that risk profiling was also done at the time of offering free trial. In addition, the Noticee, vide email dated October 27, 2022, had submitted that no free trial is offered to client. Therefore, it was observed that the Noticee is providing contradicting statements with regard to “risk profiling Questionnaire Analysis process”.

9.25 Further, the Noticee had submitted that risk profiling score was communicated to its client/s through email. In order to check the veracity of the claim made by Equity99, the Noticee was advised to provide the record of such communication for any three clients. The Noticee, vide email dated October 27, 2022, had submitted that the assessment score is immediately communicated to client/s via phone. However, the Noticee did not submit any evidence in this regard. Therefore, it was observed that no such communication was given to clients by the Noticee.

9.26 It is, therefore, alleged that the Noticee has violated the provisions of Regulation 16(b)(iii) and 16(e) of the IA Regulations, 2013.

9.27 Further, as the Noticee was not doing the risk profiling correctly, the advice offered by the Noticee under “high risk category” to such clients was not suitable to the risk profile of the clients. In other words, the Noticee recommended same services to clients falling under low, medium and high risk categories. It is therefore alleged that the Noticee has violated the provisions of Regulation 17 (a), (c) and (d) of IA Regulations, 2013 read with clauses 1 and 9 of the Code of Conduct under Regulation 15(9) of IA Regulations, 2013.

Submissions and Findings:

9.28 The Noticee, vide its reply dated November 03, 2023, had made the following submissions with respect to the charges of risk profiling and suitability:

“Risk profiling is done based on the risk profile questionnaire and interaction with the individual. Based on his current financial situation and risk tolerance level, a particular risk appetite is assigned to the clients. The same is communicated and explained to the client and only after the client agrees to the same, the service is given to the client. The same may clearly be observed from the declarations mentioned on the risk profile questionnaire (as reiterated below), which is signed and acknowledged by the client itself-

“Investment adviser has communicated to me the risk appetite score calculated form the risk profile questionnaire. The risk score and corresponding appetite has been explained to me by the investment advisor. I understand the risks involved with the investment advice provided by the Investment Adviser.

I have all the information about the products, risk factors etc., and have gone through all the relevant information about the product being advised and have sought clarification about the same.

I intend to subscribe to the services, as offered by the investment adviser after understanding all the risk factors and my risk appetite.”

Our risk profiling questionnaire is completed by our clients and is signed by them. It is important to note that the same signed copy of the risk profiling questionnaire by our clients also includes the following key points:

- We have communicated the risk appetite score calculated from the risk profile questionnaire to our clients.

- The risk score and corresponding risk appetite are explained to our clients by our investment advisor.

- Our clients acknowledge that they understand the risks associated with the investment advice provided by our Investment Adviser.

- Our clients confirm that they have been provided with all the necessary information about the products, including risk factors, and have reviewed all relevant information about the product being advised. They also state that they have sought clarification on any aspects they require.

- Clients express their intention to subscribe to our services after understanding all the risk factors and their risk appetite.

Our suitability assessment of advice is based on the risk appetite of our clients and is communicated to them before the commencement of our services. The signed risk profile questionnaire serves as validation for this process. Services are explained to our clients in conjunction with their risk appetite, and all queries and concerns expressed by our clients regarding the product’s suitability, their risk appetite, and other related matters are addressed. Only after these clarifications are provided do we proceed with delivering our services to the clients.

It is essential to recognize that the suitability of advice is not solely a function of risk appetite; it also takes into account the client’s current financial condition and risk tolerance. Clients with the same risk appetite may have different levels of risk tolerance. Therefore, the suitability of advice is not a constant function based on a single variable. As an example, consider two investors with different attributes regarding risk appetite:

- Investor A is in their 20s, has a variable income source, moderate risk appetite, has just started earning, a long working horizon, and no significant financial responsibilities. Equity investment is suitable for them.

- Investor B is in their 40s, has a stable, fixed salary, a high-risk appetite, and a secure job. Equity investment is also suitable for them based on their high, stable current income.

In this example, despite having different risk appetites, both investors find the same product suitable based on their respective financial situations and goals.

Suitability assessment.

It is imperative to understand that suitability assessment is inherently a subjective process, and each adviser employs their distinct methodology for analysing the suitability of advice provided. There are no standardized, fixed criteria for suitability assessment explicitly outlined in regulatory texts or guidelines.

The subjective nature of suitability assessment allows for the consideration of a wide range of factors, such as a client’s financial situation, goals, risk appetite and risk tolerance. This flexibility ensures that the advice provided is tailored to the unique circumstances and preferences of each client. The absence of strict, predefined criteria acknowledges the complexity of the financial advisory landscape and the need for a personalized approach.

At our organization, we employ a diligent and client-centric approach to suitability assessment, taking into account the individual attributes and requirements of each client. We are committed to ensuring that the advice we render aligns with the client’s best interests and financial objectives.”

9.29 I note that Regulation 16(b)(iii) of the IA Regulations, 2013 clearly specifies that the Investment Adviser shall ensure that it has a process for assessing the risk a client is willing and able to take, including appropriately interpreting client responses to questions and not attributing inappropriate weight to certain answers. Further, Regulation 16(e) of the IA Regulations, 2013 states that the risk profile of the client be communicated to the client after risk assessment is done. I find from the submissions made by the Noticee with respect to risk profiling that the Noticee has stated to have done the risk profiling on the basis of risk profile questionnaire and interaction with clients and the same has been communicated and explained to the client and only after the client has agreed to the same, the service has been given to the client. However, I do agree with the finding of the DA in the Enquiry Report dated November 29, 2023 that the present charge against the Noticee is not that of not undertaking risk profiling of its clients but not doing the risk profiling properly and that of improperly categorizing the risk appetite of its clients.

9.30 I find from the material available on record that as per the procedure followed by the Noticee to access the risk profile of clients, a client is categorized as a “high risk” client only if that client scores more than 14 to 21 in the risk profile questionnaire. As per the risk profile questionnaire of the Noticee “Any client with risk appetite score below 9 is classified as Low Risk Appetite Client. Any client with risk appetite score between 9 & 14 is classified as Medium Risk Appetite client and will be offered Medium Risk products / services, while a client with Risk Appetite score above 14 can select any product / service since the Risk Appetite is high”. On perusal of risk profile questionnaire forms filled by few clients, I find that the Noticee has categorized some of these clients as “high risk”, even though they have scored less than or equal to 14 in their risk profile questionnaire. I note that one of the clients, Mr. Vijay Rameshlal Lalwani, had scored 12 in his risk profiling questionnaire. However, the said client has been categorized by the Noticee under ‘high risk’ category. Further, risk profile questionnaire filled by Mr. Sunil Kumara is also available on record which shows the risk profile score to be 14. Thus, as per the abovementioned categorization mentioned in the proforma risk profile questionnaire, the said client should have been categorized under

‘Medium Risk’ category. However, I find that the said client has been categorized under ‘High Risk’ category. Therefore, I find that the Noticee has clearly not adhered with its own risk profiling policy. In view of the evidence available on record, I do not find any merit in the submissions of the Noticee with regards to the said charge. Thus, I agree with the findings of the DA in the Enquiry report and conclude that the Noticee, by not doing the risk profiling properly, has violated the provision of Regulation 16(b)(iii) of the IA Regulations, 2013.

9.31 With respect to the charge of not communicating risk profiling scores to its clients, I note that the Noticee has not provided any evidence showing communication done via emails and / or phone calls as claimed by it. Also, the DA in the Enquiry Report has even observed the Noticee to have made contradictory statements with respect to the communication of risk profiling scores to its clients. In view of the same, I agree with the findings of the DA in the Enquiry report and conclude that the Noticee, by failing to communicate the risk profiling to its clients, has violated the provisions of Regulation 16(e) of the IA Regulations, 2013.

9.32 With respect to the charge of suitability, I note that in terms of Regulation 17(a) of the IA Regulations, 2013, the investment adviser shall ensure that all the investments on which investment advice is provided is appropriate to the risk profile of the client. Further, Regulation 17(c) of the IA Regulations, 2013 states that the Investment Adviser shall ensure that it understands the nature and risk of products or assets selected for clients and Regulation 17(d) states that the Investment Adviser shall ensure that it has a reasonable basis for believing that a recommendation or transaction entered into (i) meets the client’s investment objectives, (ii) is such that the client is able to bear any related investment risks consistent with its investment objectives and risk tolerance, (iii) is such that the client has the necessary experience and knowledge to understand the risks involved in the transaction.

9.33 The Noticee, in its reply, to the enquiry SCN has stated that the suitability assessment is inherently a subjective process and each adviser employs its distinct methodology for analyzing the suitability of advice provided. Further, it has been stated that there is no standardized, fixed criteria for suitability assessment explicitly outlined in regulatory texts or guidelines and that the subjective nature of suitability assessment allows for the consideration of a wide range of factors such as a client’s financial situation, goals, risk appetite and risk tolerance. Further, the Noticee has contended that risk profiling questionnaire is completed by its clients and is signed by them and that Noticee’s suitability assessment of advice is based on the risk appetite of its clients and is communicated to the clients before the commencement of its services.

9.34 I find that it has already been established that the Noticee has failed to undertake the risk profiling of its clients properly and that it has even failed to communicate the risk profiling done at its end to its clients in violation of the provisions of Regulation 16(b)(iii) and 16(e) of the IA Regulations, 2013. Therefore, it is implied that if the risk profiling by the Noticee has not been done properly, the suitability of products / services offered by the Noticee to the client would be directly impacted. Thus, the Noticee’s argument that suitability assessment of advice was based on the risk appetite of its clients and is subjective cannot be accepted and does not hold good in the light of the fact that the Noticee has been selling high risk product to its clients, their being classified wrongly under the category of “high risk” clients. The Noticee, by undertaking the risk profiling incorrectly / improperly, has not only been selling wrong services / products to the clients which are not as per their suitability but also has been conducting its business not in the best interest of its clients.

9.35 In view of the foregoing, I agree with the findings of the DA and conclude that the Noticee has violated the provisions of Regulation 17 (a), (c) and (d) of IA Regulations, 2013 read with Clauses 1 and 9 of the Code of Conduct under Regulation 15(9) of IA Regulations, 2013.

F. Redressal of client grievances Allegation No. 7:

9.36 During the inspection, it was observed that one complaint was received against Noticee on SCORES platform from one Mr. Arun Joshi regarding loss incurred on the recommendations given by Noticee and the same is still showing ‘pending’ in SCORES. On perusal of the complaint and submission made by the Noticee during inspection, it was observed that the recommendation of stocks was made to Mr. Arun Joshi without carrying out risk profiling / KYC / agreement. It was further observed that the said complaint is yet to be resolved by the Noticee. In view of the same, it is alleged that the Noticee has failed to redress client grievance promptly thereby violating the provisions of Regulation 21(1) of the IA Regulations, 2013.

Submissions and Findings:

9.38 The Noticee, in its reply dated November 03, 2023 to the enquiry SCN has provided the timelines within which steps were taken by the Noticee to resolve the complaint pending on SCORES platform which is as under:

- Complaint received from SEBI for Resolution- July 13, 2022.

- Action Taken Report (ATR) filed by us on SCORES- August 08, 2022.

- Complaint sent to complainant for clarification- October 06, 2022.

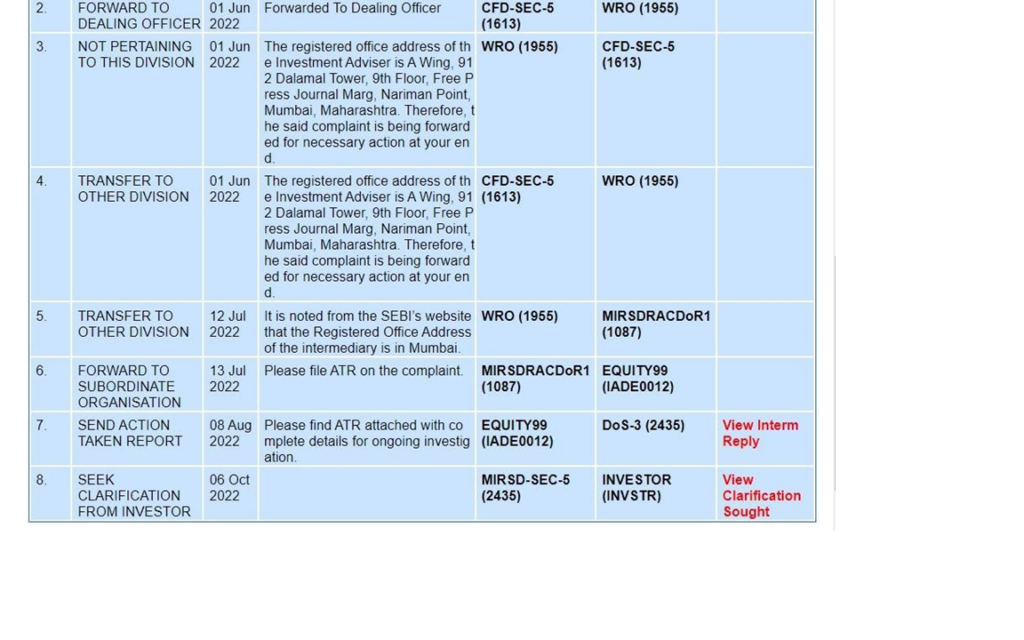

9.38 Further, it has been submitted by the Noticee that post filing of the ATR on SCORES, the complaint was forwarded to the complainant for clarification. However, no clarification was received from the complainant. Further, the Noticee also stated that it tried to connect with the complainant for responding to the clarifications sought but the complainant did not respond. Therefore, it is the case of the Noticee that the complaint is pending on the SCORES platform at complainant’s end and not at its end. The screenshot provided by the Noticee of the complaint history on SCORES portal is as under:

9.39 I note that the complaint was forwarded to the Noticee by SEBI on July 13, 2022 and the Noticee had, within the prescribed timelines, had filed an ATR on the complaint on August 08, 2022. Thereafter, clarification was sought by SEBI from the complainant on October 06, 2022. However, from the record available, I find that no clarification has been provided by complainant till date. Considering the prompt actions taken by the Noticee on the SCORES platform for redressing the complaint by filing ATR within the timelines and also by taking steps to contact the complainant to resolve the complaint, I agree with the finding of the DA that the Noticee has tried to redress the client’s grievance promptly and therefore, I am inclined to conclude that the Noticee cannot be held liable for violating the provisions of Regulation 21(1) of the IA Regulations, 2013. Therefore, the said charge does not stand established against the Noticee.

G. Know your Client procedures Allegation No. 8

9.40 Upon inspection, it was observed that since taking registration from SEBI in the year 2016, the Noticee had not obtained registration with CDSL Ventures Limited and NSDL Database Management Limited (NDML) and KYC Registration Agencies (KRAs) which was mandatory for following the Know Your Client (KYC) procedure as specified by SEBI from time to time. Thus, it has been alleged that the Noticee has violated the provisions of Regulation 15(8) of IA Regulations, 2013.

Submissions and Findings:

9.41 I find from the submissions made by the Noticee before the DA with respect to the said charge that it has admitted that at the time of inspection, it did not have NDML and CKYC registrations. Thus, the Noticee by not complying with the KYC procedures has violated the provisions of Regulation 15(8) of the IA Regulations, 2013. However, it is noteworthy that the Noticee has now taken corrective steps by taking NDML registration and the CKYC registration is underway.

H. Display of Mandatory Information Allegation No. 9

9.42 During inspection, SEBI officials had visited the registered office of the Noticee. During the visit, it was observed that the Noticee had not displayed the name and contact details of the Compliance Officer in its office in terms of the SEBI Circular No. CIR/MIRSD/3/2014 dated August 28, 2014. Thus, it is alleged that the Noticee has violated Clause 2 of SEBI Circular CIR/MIRSD/3/2014 dated August 28, 2014 and Regulation 15(9) of IA Regulations, 2013 read with Clause 8 of the Code of Conduct as specified in Third Schedule of IA Regulations, 2013.

Submissions and Findings:

9.43 With respect to the said charge, the Noticee, vide its reply before the DA has pleaded lack of awareness about certain regulatory requirements, including the display of the name and contact details of the compliance officer in its office. Further, the Noticee has enumerated certain corrective measures taken by it to avoid such regulatory non-compliances. The submissions made by the Noticee are reproduced as under:

“It is with self-effacement that we acknowledge our previous lack of awareness about certain regulatory requirements, including the display of the name and contact details of the compliance officer in our office. However, we have taken swift corrective action to rectify this oversight by ensuring that the compliance officer’s information is now prominently displayed.

We want to emphasize that while we acknowledge that our prior unawareness is not an excuse for the oversight, the ultimate objective of this regulatory requirement is to ensure that our clients are informed about the grievance redressal process. It is essential to provide our clients with the means to raise queries or complaints effectively through proper communication channels.

To this end, we have established a Grievance Redressal Mechanism page on our website. This page not only outlines the redressal process within our organization but also provides details about the SCORES portal for filing complaints. Same may be accessed through below link-

https://www.equity99.com/Investor–Grievances–Redressal

We believe that this comprehensive approach ensures that our clients have clear and accessible avenues to address any concerns or grievances.”

9.44 I note that SEBI has been taking various measures to create awareness among investors about grievance mechanisms available to them through workshops as well as through print and electronic media. In order to serve better, SEBI vide its Circular dated August 28, 2014 came up with an additional measure by mandating the offices of all SEBI registered intermediaries to prominently display basic information such as name of the compliance officer, contact number of the said person, etc. for the purpose of grievance redressal mechanism available to investors. The said information was to be displayed by all the SEBI registered intermediaries within 60 days from the date of the said SEBI Circular. The Noticee has also admitted to the said violation. In view of the above, I conclude that the Noticee, by not displaying the requisite information during the inspection, has violated the provisions of Clause 2 of SEBI Circular CIR/MIRSD/3/2014 dated August 28, 2014 and Regulation 15(9) of IA Regulations, 2013 read with Clause 8 of the Code of Conduct as specified in Third Schedule of IA Regulations, 2013. However, it is noteworthy to state that the Noticee, has taken corrective steps and has now complied with the said provisions.

I. Display of investor charter and disclosure of Investor Complaints

Allegation No. 10

9.45 On examination of website of the Noticee, it was observed that the Noticee had displayed the investor charter and details of the investor complaints on its website. Under the heading “Trend of annual disposal of complaints,” it is noted that the Noticee has displayed 0 complaints from 2018-2021. However, SEBI share portal shows receipt of one complaint in 2018 and two complaints in 2019. Thus, it is alleged that the Noticee, by not displaying correct information, has violated Clause 3 of the SEBI circular SEBI / HO / IMD / IMD-II CIS / P / CIR / 2021 / 0686 dated December 13, 2021.

Submissions and Findings:

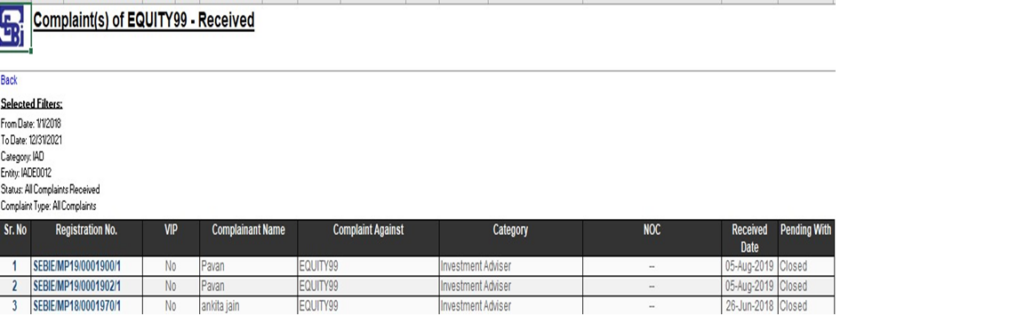

9.46 I note that the SEBI share portal shows receipt of one complaint in the year 2018 and two complaints in the year 2019 against the Noticee. The details of the same are as under:

9.47 I note from the submissions of the Noticee before the DA that as stated by the Noticee, total two complaints were filed against Noticee during the entire tenure of its registration and there was only 1 complaint in the time period 2018-2021, as shown hereunder (screenshot- as provided by the Noticee):

9.48 The Noticee has stated that one of the two complaints was withdrawn by the complainant without any response from the Noticee. Considering the same, it is the case of the Noticee that the withdrawn complaint should not be counted for the disclosure purposes. Further, with respect to the remaining complaint, the Noticee states that the said complaint was received by it on July 12, 2022 and therefore, there were no valid complaints filed against the Noticee during the fiscal years 2018-2021. I find that there is a mis-match between the total number of complaints as displayed on the SEBI share portal and the information provided by the Noticee from the SCORES portal. Considering the same and based on the evidence provided by the Noticee, I find it appropriate to give benefit of doubt to the Noticee and agree to the submissions made. However, I do not agree to the submission that only because one complaint was withdrawn by the complainant, the said complaint should not be considered for the purposes of disclosure.

9.49 I note that in terms of SEBI Circular dated December 13, 2021, in order to further enhance transparency in grievance redressal, the Investment Advisors are under an obligation to disclose the details of investor complaints by 7th of the succeeding month in the revised format provided in the said Circular on a monthly basis. Therefore, the said circular clearly puts a statutory obligation on the Investment Advisors to make the disclosures with respect to the investor complaints. Further, no exemption from adhering with the said compliance has been provided in the said circular. In the light of the same, I agree with the finding of the DA in the Enquiry Report dated November 29, 2023 and conclude that the Noticee was under an obligation to display one complaint received by it and by failing to do the same, the Noticee is in violation of the provisions of Clause 3 of the SEBI Circular No. SEBI/HO/IMD/IMD-II CIS/P/CIR/2021/0686 dated December 13, 2021.

10. From the foregoing, it is well established and therefore, concluded that the Noticee has violated the following provisions of law:

(a) By failing to validate and renew the NISM certification which expired on April 01, 2022, the Noticee has violated the provisions of Regulation 15(13) read with Regulation 7(2) of the IA Regulations, 2013,

(b) By failing to include the word ‘Investment Advisor’ in its name, the Noticee has violated the provisions of Regulation 13(a) and (c) of the IA Regulations 2013 read with Clause 8 & 9 of the Code of Conduct as specified in Third Schedule of IA Regulations, 2013,

(c) By collecting fees and giving investment advice before entering into agreements with its clients, the Noticee has violated the provisions of Regulation 19 (1) (d) of IA Regulations, 2013 read with Clause (ii)(c) of SEBI Circular no. SEBI/HO/IMD/DF1/CIR/P/2020/182 dated September 23, 2020,

(d) By distributing / circulating research reports to its Telegram Channel subscribers for consideration without obtaining a certificate of registration as a Research Analyst, the Noticee has violated the provisions of Regulation 3(1) of the RA Regulations, 2014.

(e) By displaying incorrect information on its website with respect to the qualification of team members, the Noticee has violated the provisions of Regulation 15(9) of IA Regulations, 2013 read with Clauses 1,2 5,8 & 9 of Code of Conduct as specified in Third Schedule of IA Regulations, 2013.

(f) By not undertaking risk profiling of its clients properly and not providing products/ schemes suitably to its clients based on their risk appetite, the Noticee has violated the provisions of Regulation 16 (b) (iii), 16 (e), Regulation 17 (a), (c) and (d) of IA Regulations read with clauses 1 and 9 of Code of Conduct under Regulation 15(9) of the IA Regulations, 2013.

(g) By not taking registration with NDML and with KYC registration agencies during the period of inspection, the Noticee has violated the provisions of Regulation 15(8) of IA Regulations, 2013.

(h) By not displaying the name and contact details of the Compliance Officer at its registered office, the Noticee has violated Clause 2 of SEBI Circular CIR/MIRSD/3/2014 dated August 28, 2014 and Regulation 15(9) of IA Regulations, 2013 read with Clause 8 of the Code of Conduct as specified in Third Schedule of IA Regulations, 2013.

(i) By not displaying the investor complaints on its website correctly, the Noticee has violated the provisions of clause 3 of the SEBI circular SEBI/HO/IMD/IMD-II CIS/P/CIR/2021/0686 dated December 13, 2021.

11. I note that Section 12(3) of the SEBI Act, 1992 empowers SEBI to either suspend or cancel the certificate of registration of the entity in a manner that may be determined by the regulations. I find that the DA in the Enquiry Report dated November 29, 2023, while observing that the aforementioned violations have been established against the Noticee, has taken into account the corrective steps taken by the Noticee in order to comply with the statutory requirements and has taken a lenient view by recommended issuance of regulatory censure against the Noticee. However, I am of the view that being a SEBI registered intermediary, the Noticee has higher responsibility to adhere and comply with all the statutory requirements and cannot plead ignorance of law and / or inadvertent lapses. It is pertinent to mention that despite initiation of the present proceedings against the notice, the Noticee has not taken any steps and / or produced any documentary evidence to show that it is in the process of getting its certification renewed. Further, with respect to communicating the risk profiling with the clients as required under the IA Regulations, I find that the Noticee not only has not produced any documentary evidence to place on record compliance but has made contradictory statements which clearly shows the casual approach of the Noticee towards the regulatory enforcement proceedings.

12. In the light of the foregoing, I am of the firm view that, for the aforementioned violations established against the Noticee, a direction of suspension of certificate of registration for a period of three months or until the time the Principal Officer of the Noticee i.e. Mr. Rahul Sharma renews the requisite NISM certification in accordance with Regulation 7 of the IA Regulations, 2013, whichever period is higher, seems to be appropriate against the Noticee.

ORDER AND DIRECTIONS

13. In view of the above, I, in exercise of the powers conferred upon me in terms of Section 12(3) and Section 19 of the SEBI Act, 1992 read with Regulation 27(5) of the Intermediaries Regulations, 2008, hereby direct that the Certificate of Registration granted to the Noticee viz. Equity99 (SEBI Registration No. INA000005358) is suspended for a period of three months or until the time the Noticee (Principal Officer – Mr. Rahul Sharma) renews the requisite NISM certification in accordance with Regulation 7 of the IA Regulations, 2013, whichever period is higher.

14. The above direction shall come into force with immediate effect.

15. A copy of this Order shall be served on the Noticee, BASL, on all the recognized Stock Exchanges and Depositories.

Date: January 24, 2024 Dr. ANITHA ANOOP

Place: Mumbai CHIEF GENERAL MANAGER

SECURITIES AND EXCHANGE BOARD OF INDIA